Summary:

This blog post unveils the significance of annuity tables in financial planning. It delves into the mathematical foundation behind annuities, showcasing formulas for both future and present values. Emphasizing the importance of the Future Value Factor and the Rate Table for the Future Value of an Ordinary Annuity of 1, the post offers insights into optimizing annuity investments. Real-life success stories inspire readers, highlighting the transformative power of annuities. With keywords like “discount rate,” “rate of return,” and “types of annuities,” the article encourages readers to harness annuities for a secure financial future.

Introduction

Annuity tables, often seen as the compass in this maze, are pivotal tools in financial planning. They’re the bridge between your current financial status and your future aspirations. With these tables, you can visualize the impact of interest rates and time on your investments, making retirement planning, loan payments, and investment decisions a breeze. Dive in with us as we demystify the world of annuity tables, helping you make informed decisions and achieve your financial goals with ease.

1. About Annuity Tables

A. What Is an Annuity Table and How Do You Use One?

An annuity table, at its core, is a reference chart. It provides the present or future value of a series of equal payments made at regular intervals. Think of it as a roadmap that shows you how much a sum of money will be worth in the future, or how much you need today to achieve a certain amount in the years to come.

But why is it so significant in financial planning? Imagine planning a trip without a map or GPS. You might get to your destination, but the journey would be fraught with uncertainty and potential pitfalls. Similarly, in the journey of financial planning, an annuity table acts as that essential map, guiding you towards a more secure financial future. It helps individuals and financial professionals alike to make informed decisions about investments, retirement planning, and more.

2. Diving Deep into the Formulas

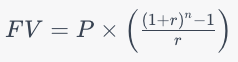

A. Formula and Calculation of the Future Value of an Annuity

Ever wondered how financial experts predict the future value of your investments? The secret lies in the mathematical foundation of annuities.

An annuity consists of consistent payments made at uniform time periods. The formula to calculate the future value of an annuity is:

Where:

- FV is the future value of the annuity.

- P is the periodic payment.

- r is the interest rate per period.

- n is the number of periods.

Let’s simplify it. Imagine you invest $100 every month at an interest rate of 5% annually for 10 years. Using the formula, the future value of your investment would be approximately $15,528.64. That’s the power of compound interest working in your favor!

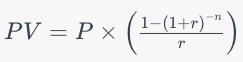

B. How To Use the Present Value of an Annuity Formula

Have you ever thought about the worth of your future investments in today’s terms? That’s where the present value of an annuity comes into play. It’s the inverse of the future value. In simpler terms, it tells you what a future series of payments is worth in today’s dollars.

The formula is:

Where:

- PV is the present value of the annuity.

- P, r, and n have the same definitions as above.

To determine the present value of your annuity, follow these steps:

- Identify the periodic payment, interest rate, and number of periods.

- Plug the values into the formula.

- Calculate to get the present value.

For instance, if you’re set to receive $100 every month for the next 10 years with a 5% annual interest rate, the present value would be approximately $9,129.41.

3. Understanding Key Components

A. Future Value Factor: Its Role and Importance

Have you ever been intrigued by how your investments grow over time? The magic behind this growth is often attributed to the Future Value Factor. At its essence, the Future Value Factor is a pivotal concept in annuities, helping determine the future value of regular payments or investments over a specific period. It takes into account the interest rate and the time period, considering the compounding effect of interest on the annuity payments.

But why should you care? Imagine planting a seed and watching it grow into a tree. The Future Value Factor is akin to the nutrients and water that influence the tree’s growth. Similarly, this factor influences the value of your annuity, allowing you to foresee how your contributions will flourish over time.

B. Rate Table For the Future Value of an Ordinary Annuity of 1

It represents a method for determining the future value of an annuity. This table contains a factor specific to the future value of a series of payments when a certain interest earnings rate is assumed. By multiplying this factor by one of the payments, you can determine the future value of the stream of payments.

For instance, if you plan to make 5 payments of $10,000 each into an investment fund with an interest rate of 6%, the factor, as noted in certain tables, would be 5.6371. Multiplying the 5.6371 factor by $10,000 gives you a future value of the annuity of $56,371.

But what’s the significance of the “Ordinary Annuity of 1” in these calculations? It’s a standardized measure, ensuring that the calculations are consistent and reliable.

4. Navigating the Future Value Annuity Table Like a Pro

A. Step-by-Step Guide: Making Sense of the Numbers

What if I told you that with a few simple steps, you can master this table and make it work for your financial advantage?

Beginner’s Guide to Reading and Understanding the Table:

- Start Simple: Begin with the basics. Identify the interest rate and the number of periods. These are your primary guides.

- Locate Your Factors: Once you’ve identified the above, locate the corresponding factor in the table. This factor will be crucial for your calculations.

- Apply the Formula: Future Value = Annuity Payment x Factor from the table. Sounds simple, right?

Tips for Accurate Future Value Calculations:

- Stay Updated: Financial landscapes change. Ensure you’re using the most recent table for accurate results.

- Double-Check: A small error can lead to significant miscalculations. Always double-check your numbers.

B. Advanced Strategies: Optimizing Your Annuity Investments

The Future Value Annuity Table isn’t just a tool for calculations; it’s a roadmap to maximizing your returns.

How to Leverage the Future Value Annuity Table for Maximum Returns:

- Diversify: Don’t put all your eggs in one basket. Spread your investments across different interest rates and periods.

- Stay Informed: The world of finance is ever-evolving. Keep abreast of the latest trends and adjust your strategies accordingly.

Expert Insights and Recommendations:

- Consult a Financial Advisor: They have the experience and knowledge to guide you towards the best decisions for your financial future.

- Educate Yourself: The more you know, the better your decisions. Attend seminars, read books, and stay updated.

5. Real-Life Success Stories

A. From Novice to Expert: Journey of Annuity Investors

We often hear tales of rags to riches, but how often do we come across stories of financial novices turning into savvy annuity investors? Let’s delve into some inspiring tales that highlight the transformative power of annuities.

Inspiring Stories of Individuals Who Benefited from Annuities:

Meet Frankie and Linda: Their journey began in 2011, much like yours, trying to find the right way to distribute retirement assets. They explored various options, and after thorough research, they decided to invest in annuities. Over a span of seven years, their combined assets grew from $500,000 to a whopping $763,000, translating to more than a 6% annualized return, all without any risk of loss. Their secret? Flexibility in reinvestment and a keen eye for identifying opportunities.

Another testament to the power of annuities comes from a Kiplinger article, which emphasizes the importance of annuities as a hedge against longevity risk. With people living longer, the fear of outliving one’s savings is real. Annuities, with their guaranteed income, act as a safety net, ensuring you have a steady flow of income, irrespective of market fluctuations.

Lessons Learned and Tips for New Investors:

- Stay Updated: The financial landscape is ever-evolving. Ensure you’re equipped with the latest knowledge.

- Diversify: Don’t rely solely on one financial instrument. A mix of investments can help mitigate risks.

- Consult Experts: While it’s essential to do your research, consulting a financial advisor can provide insights tailored to your needs.

Annuities have proven to be a game-changer for many. Their stories are not just tales of financial success but are also about foresight, diligence, and the will to secure one’s future. So, are you ready to pen your success story with annuities?

Conclusion

Navigating the intricate world of annuities can be daunting, but as we’ve journeyed through, the rewards are evident. Whether you’re deciphering the discount rate, aiming for an optimal rate of return, or choosing between the myriad types of annuities, the goal remains clear: securing a financially stable future. Remember, a regular annuity can be your ticket to consistent, guaranteed returns, acting as a safety net in an unpredictable financial landscape. But, like any investment, the key lies in understanding, diligence, and making informed decisions. So, as you stand at the crossroads of financial planning, ask yourself: Are you ready to harness the power of annuities and maximize your returns? Dive deeper, explore more, and let annuities be the cornerstone of your financial blueprint. Take action now — consult a financial expert and ensure your money works as hard for you as you did for it.

Frequently Asked Questions (FAQ)

1. What are the primary differences between immediate and deferred annuities?

Immediate annuities start payments almost immediately after a lump sum is paid, typically within a year. Deferred annuities, on the other hand, accumulate money for a period before starting to pay out. This period can be several years, allowing the investment to grow.

2. Are annuities protected against inflation?

Standard annuities do not offer protection against inflation. The amount you receive remains fixed, which might decrease in real value over time due to inflation. However, some annuities offer an inflation-protection option, usually at a higher initial cost.

3. Can I withdraw money from my annuity before its maturity?

Yes, you can withdraw money from an annuity before its maturity, but it may come with penalties or surrender charges. Additionally, if you withdraw before the age of 59½, you might face additional tax penalties.

4. How are annuities taxed?

Annuities grow tax-deferred. When you make withdrawals or receive payments, the earnings (but not the principal) are taxed as ordinary income. If you withdraw funds before age 59½, there might be an additional 10% early withdrawal penalty.

5. What happens to my annuity if I pass away before it matures?

If you pass away before the annuity starts paying out, most contracts guarantee that your beneficiary will receive at least the amount of the payments you’ve made into the annuity. Some annuities also offer a death benefit option, which might provide your beneficiary with a larger payout.