Summary:

This blog post explores the essential aspects of ERISA plans to secure a mother’s financial future. It sheds light on the importance of understanding Employee Benefit Plans and the crucial role of disclosure requirements. The blog also emphasizes the significance of Employee Organizations and Independent Agencies in managing ERISA plans. It explores the differences between Employee Welfare Benefit Plan and Employee Pension Benefit Plan, providing guidance on choosing the right plan. Furthermore, the article delves into the concept of Percent of Plan Assets and its impact on beneficiaries. It provides an overview of the Townsend Plan and how it might fit into a retirement strategy. Lastly, the role of Insurance Arrangements in ERISA-covered Retirement Plans is discussed. The post is a comprehensive guide for those looking to secure a sound financial future for their mothers through ERISA plans.

Introduction

It’s often said that a mother’s love is irreplaceable and immeasurable. From nurturing us in our early years to being our support system in adulthood, our mothers play a vital role in our lives. But as we grow older, roles often reverse, and the question arises — how can we ensure their comfort and financial security in their golden years? This question is especially pressing in the face of increasing medical expenses and the potential for financial uncertainty in retirement.

Here, the importance of thoughtful retirement planning comes into play. And one significant player in this realm is the Employee Retirement Income Security Act (ERISA) covered retirement plan. It’s a tool that, when used correctly, can ensure a stable financial future for your loved ones, particularly your mother.

This blog post delves into how an ERISA-covered retirement plan can secure your mother’s financial future. We’ll explore the benefits of such a plan, understand how to make your mother a beneficiary, and offer tips to maximize those benefits.

1. The Critical Role of Mothers in Our Lives

A. Acknowledging Your Mother’s Contributions

Our mothers often put our needs above their own, sacrificing her time, energy, and sometimes even her ambitions, to ensure we thrive. In the face of increasing medical costs and the often unpredictable nature of retirement, it’s crucial to recognize these contributions and repay our mothers’ love and dedication with the promise of a secure future.

B. The Importance of Ensuring Financial Security for Your Mother

Unfortunately, for many retirees today, this dream is overshadowed by the fear of financial instability. Rising living costs, coupled with the looming uncertainty of medical expenses, can make retirement a source of anxiety rather than relief.

When it comes to our mothers, these fears are amplified. Having spent a significant portion of their lives caring for others, they might not have had the same opportunities to secure their own financial futures.

By making your mother a beneficiary of your ERISA-covered retirement plan, you can provide her with a consistent income stream in her golden years. This not only ensures her day-to-day expenses are covered, but also gives her the means to handle unexpected costs such as medical bills or emergency expenses.

2. Understanding ERISA-Covered Retirement Plans

A. What is an ERISA-Covered Retirement Plan?

The Employee Retirement Income Security Act (ERISA), passed in 1974, has one main goal — to protect the individual’s retirement assets. In essence, ERISA is a law that provides safeguards to ensure that your employer is upholding their fiduciary responsibility in managing the retirement plans they offer.

Common ERISA-covered plans include 401(k) plans, traditional pension plans (also known as defined benefit plans), and some types of Individual Retirement Accounts (IRAs).

B. How ERISA-Covered Plans Benefit Your Mother as a Beneficiary

In an ERISA-covered plan, a spouse is the default beneficiary. However, if you’re unmarried, or if your spouse has given written consent, you can name another individual — like your mother — as a beneficiary. By naming your mother as a beneficiary of your ERISA-covered retirement plan, you can create a long-term source of income for her.

Upon your passing, the retirement benefits would then be transferred to your mother. Depending on the type of plan and its specific rules, your mother could either receive lump-sum payments or choose to receive the benefits as annuity payments over a specific period.

Securing your mother’s financial future through your ERISA-covered plan not only provides her with monetary security but also gives her peace of mind especially when it comes to unforeseen medical expenses.

ERISA plans, with their robust protections and flexibility in beneficiary designation, serve as a lifeline in retirement planning, a tool for ensuring our loved ones are taken care of even when we are no longer there to do it ourselves.

3. The Financial Challenges Faced by Retiree Mothers

A. The Rising Cost of Medical Expenses for Retiree Mothers

One of the most pressing financial challenges that retiree mothers face is the rising cost of medical expenses. As we age, our medical needs tend to increase, and with that comes a surge in healthcare expenses. In a study conducted by Fidelity, an average retired couple aged 65 in 2022 needed around $300,000 to cover healthcare expenses throughout retirement. And with medical inflation outpacing general inflation, these costs are expected to increase further.

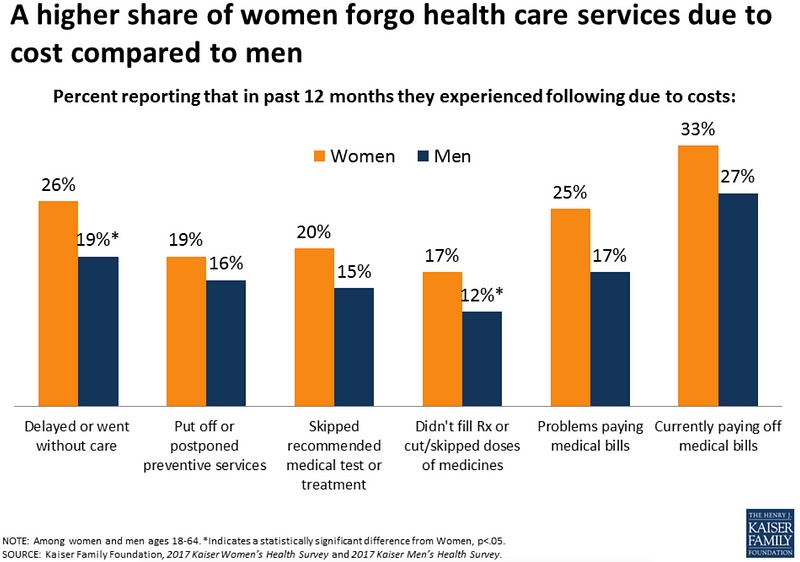

This scenario poses an even greater challenge for our mothers. Due to the longevity gap, women are expected to live longer than men, and this longevity translates into a longer period of healthcare needs. From routine check-ups and medications to potential long-term care needs, our mothers are likely to face significant medical expenses during their retirement years. An ERISA-covered retirement plan can serve as a safety net, helping to shoulder these costs and ensuring that our mothers receive the medical care they deserve.

Figure Legend: More women avoid health care services because of cost than men.

B. The Fear of Financial Insecurity for Your Mother

Alongside escalating medical expenses, another significant concern for retiree mothers is the fear of financial insecurity. Many of our mothers may have taken time off from their careers for family obligations, resulting in fewer years of income generation and less savings for retirement. Additionally, with the rising cost of living, their savings may not stretch as far as they’d hoped. This can cause financial anxiety and have detrimental effects on mental health, leading to increased stress and worry.

However, there is a way to alleviate these fears. By naming your mother as a beneficiary in your ERISA-covered retirement plan, you can help provide a financial buffer for her retirement years.

4. Making Your Mother a Beneficiary in Your ERISA-Covered Retirement Plan

A. Why Your Mother Should Be a Beneficiary

You’ve likely heard the phrase “put your money where your love is”. When it comes to your mother, ensuring her financial stability in retirement is one of the most significant ways you can express that sentiment. By making your mother a beneficiary of your ERISA-covered retirement plan, you’re providing her with a financial cushion that could greatly enhance her quality of life in her golden years.

If your mother didn’t work enough to earn the required Social Security credits or if her retirement benefits are considerably less than yours, she might be eligible to receive benefits as a dependent on your record. These additional funds, coupled with the benefits from your ERISA-covered retirement plan, could dramatically improve her financial situation during retirement.

B. Step-by-Step Process to Designate Your Mother as a Beneficiary

So, you’ve decided to make your mother a beneficiary of your ERISA-covered retirement plan. The question now is, how do you go about it? Here’s a step-by-step guide:

- Consult Your Plan Administrator: Every retirement plan has different rules for designating beneficiaries. Consult with your plan administrator to understand these rules and discuss your intention to name your mother as a beneficiary.

- Spousal Consent: If you’re married, you may need your spouse’s consent to name another person as your primary beneficiary. This rule varies from plan to plan, so make sure to clarify this with your plan administrator.

- Fill Out the Beneficiary Designation Form: Your plan administrator will provide you with a form to designate or change your beneficiary. Fill this out, making sure to correctly enter your mother’s personal information.

- Submit the Form: After you’ve filled out the form, submit it to your plan administrator. You should receive a confirmation that your beneficiary designation has been updated.

- Regular Updates: It’s a good idea to review and update your beneficiary designations periodically or after major life events.

Taking these steps can ensure a financially secure future for your mother, giving her the peace of mind she deserves in her retirement years.

5. Maximizing the Benefits of ERISA-Covered Retirement Plan for Your Mother

A. Strategic Fund Allocation for Your Mother’s Financial Security

With your mother now listed as a beneficiary of your ERISA-covered retirement plan, the next step is making strategic decisions about fund allocation. This means distributing the investments in your retirement plan to strike a balance between risk and return, bearing in mind your mother’s financial needs.

One approach you could consider is a ‘bucket’ strategy, which involves dividing retirement savings into different ‘buckets’ based on when you’ll need the funds. For example, the first ‘bucket’ could consist of money market funds and short-term bonds, providing a steady income stream for your mother’s immediate needs.

The second ‘bucket’ might contain long-term bonds and large-cap stocks, designed for use in the mid-term. Finally, the third ‘bucket’ could contain riskier assets like small-cap stocks or emerging market funds, intended for use in the far future.

By following this strategy, you can ensure your mother has access to funds when she needs them, while still benefiting from potentially higher returns in the long run.

B. Balancing Risk and Reward for Your Mother’s Peace of Mind

Many financial advisors recommend a conservative investment strategy for retirement funds, particularly for seniors who depend on these funds for their daily needs. This approach typically involves a diversified portfolio with a mix of stocks, bonds, and other low-risk investments.

However, remember that every person’s situation is unique. Therefore, it’s essential to assess your mother’s financial situation, her risk tolerance, and her long-term needs before deciding on an investment strategy. Consulting a financial advisor can be very beneficial in this regard.

C. Long-Term Care and Disability Insurance: Added Security for Your Mother

An ERISA-covered retirement plan is just one piece of the puzzle. To fully protect your mother’s financial well-being in retirement, you might also consider long-term care and disability insurance.

Long-term care insurance covers the cost of care services that aren’t covered by regular health insurance, such as assisted living, nursing home care, and home healthcare. This can be particularly beneficial for elderly individuals who may require these services in their later years.

On the other hand, disability insurance provides income protection in the event of a disability that prevents your mother from working. While this may not seem as relevant for retirees, some policies also cover care services, making it an additional layer of protection for your mother.

6. Case Studies: Securing Mothers’ Financial Future with ERISA Plans

A. Success Stories of Mothers as Beneficiaries

It can be quite impactful to learn from the real-life experiences of others. Let’s explore a couple of success stories where ERISA-covered retirement plans played a crucial role in securing the financial future of beneficiaries’ mothers.

The Smiths: John Smith, a 50-year-old engineer, decided to name his 75-year-old mother, Jane, as the primary beneficiary of his ERISA-covered 401(k) plan. With a well-diversified investment portfolio, John’s plan saw robust growth over the years. After John’s unexpected demise, Jane began receiving distributions from the plan, ensuring she could cover her living and medical expenses without relying on anyone else. This well-planned strategy gave Jane financial independence, a testament to the potential benefits of such a beneficiary designation.

The Garcias: Carlos Garcia, a single, 40-year-old teacher, designated his 68-year-old mother, Maria, as his primary beneficiary in his ERISA-governed pension plan. With careful investment and pension management, Carlos ensured that his mother would have a regular monthly income stream if something were to happen to him. When Carlos unexpectedly passed away, Maria was able to access these pension benefits, providing her with a reliable income source to cover her regular expenses and maintain her quality of life.

B. Learning from Common Mistakes in Beneficiary Designation

Just as there are success stories, there are also lessons to be learned from those who made common mistakes in their ERISA plan beneficiary designations.

The Johnsons: Bill Johnson named his mother, Emma, as the primary beneficiary of his 401(k) plan. However, he failed to update the designation after Emma’s passing. As a result, the assets of the plan went through probate, a lengthy and costly process, before being distributed according to his will.

The Andersons: Mike Anderson named his mother, Ruth, as the beneficiary of his pension plan but failed to provide a contingent or secondary beneficiary. When both Mike and Ruth passed away in a tragic accident, Mike’s assets also had to go through probate. It could have been avoided if Mike had named a contingent beneficiary.

These case studies demonstrate the potential benefits and pitfalls of naming your mother as a beneficiary in your ERISA-covered retirement plan.

7. Decoding the Jargon: Key Terms in ERISA-Covered Retirement Plans

A. What is an Employee Benefit Plan?

In the simplest terms, an Employee Benefit Plan is a retirement or welfare plan set up by an employer, an employee organization (like a union), or both, to provide retirement income or health benefits to their employees. These plans, regulated by the Employee Retirement Income Security Act (ERISA), form a vital part of America’s retirement system1.

B. Employee Benefit Plan and Your Mother’s Financial Security

An Employee Benefit Plan promises your mother a steady flow of income, even when you’re not there to provide it. ERISA-covered Employee Benefit Plans step in as your silent partners, ensuring your mother doesn’t bear the brunt of life’s unexpected turns.

C. The Role of Disclosure Requirements in ERISA Plans

The Employee Retirement Income Security Act (ERISA) requires plan administrators to provide participants and beneficiaries with certain information about their plans, including plan features and funding. This information must be provided through regular disclosure documents that are free of charge. These documents help your mother, have a clear picture of the plan’s operations, finances, and overall health. It provides a sense of control and empowerment, a feeling of being in the driver’s seat of your own financial future.

D. What is an Employee Organization?

An Employee Organization refers to labor unions or any employer association. These entities typically represent workers’ interests and play an instrumental role in negotiating employee benefit plans, including ERISA-covered plans.

E. Understanding the Townsend Plan

Named after Dr. Francis Townsend, a political activist from the early 20th century, the Townsend Plan initially aimed to ensure financial security for the elderly during the Great Depression. While not directly related to ERISA, understanding its principles can expand your perspectives on retirement planning. Think of it as an old family recipe; not often used, but potentially bringing a unique flavor to your mother’s financial future.

In its original form, the Townsend Plan proposed a monthly payout to seniors over the age of 60. This payout was contingent on the recipients spending the money within the month, thus stimulating economic activity.

F. The Role of Insurance Arrangements in ERISA-covered Retirement Plans

Insurance arrangements within ERISA plans serve a critical purpose: they provide financial security to beneficiaries against unforeseen circumstances. In the context of ERISA, an insurance arrangement typically implies that a portion of the retirement plan’s assets is invested in insurance contracts.

Conclusion

In the maze of ERISA plans, it’s the light of knowledge that guides us to make the most prudent decisions. It’s crucial for every beneficiary, like your mother, to grasp the dynamics of disclosure requirements, understand the significance of employee organizations, recognize the role of independent agencies, distinguish between Employee Welfare and Pension Benefit Plans, grasp the concept of percent of plan assets, fathom the nuances of the Townsend Plan, and navigate the currents of insurance arrangements.

Remember, the clarity of this understanding could mean the difference between a peaceful retirement and one fraught with financial anxiety!

Frequently Asked Questions (FAQ)

What is the difference between an Employee Welfare Benefit Plan and an Employee Pension Benefit Plan?

An Employee Welfare Benefit Plan provides benefits such as health insurance, disability benefits, and unemployment benefits. On the other hand, an Employee Pension Benefit Plan is aimed at providing retirement income or deferring income until termination of covered employment.

What is the significance of the Percent of Plan Assets in ERISA plans?

The Percent of Plan Assets signifies the share of the plan’s assets allocated to each beneficiary. Understanding this concept is crucial because it directly affects the financial benefits the beneficiary will receive from the plan.

What is the role of Independent Agencies in ERISA plans?

Independent Agencies such as the Department of Labor (DOL) and the Internal Revenue Service (IRS) play critical roles in regulating and overseeing ERISA plans to ensure compliance with federal laws and protection of beneficiaries.

What is the Townsend Plan and is it suitable for my mother?

The Townsend Plan is a specific kind of pension plan. Its suitability depends on individual circumstances, such as financial goals, age, and risk tolerance. It’s recommended to consult a financial advisor for personalized advice.

How do Insurance Arrangements work in ERISA-covered Retirement Plans?

Insurance arrangements provide a level of protection for the plan’s assets. In ERISA plans, insurance is often used to provide annuity options or protect against the loss of benefits in case the plan is terminated. These arrangements can provide additional security for beneficiaries.