Summary:

Explores the unique challenges women face in retirement planning, from the gender wage gap and longevity risk to elevated healthcare costs. Despite these hurdles, women have the power to take control of their financial future with a strategic and comprehensive approach.

The blog emphasizes the role of savings strategies in ensuring a comfortable retirement, including making the most of employer-sponsored retirement plans, IRAs, and maximizing social security benefits. It further highlights the importance of insurance products, such as long-term care insurance and life insurance, in securing women’s retirement.

The article also delves into estate planning, underscoring the need for women to be informed about wills, trusts, and estates to ensure their wealth is preserved and passed on to their heirs as desired. Lastly, the blog underscores the vital role a financial advisor can play in retirement planning, guiding women to make informed decisions that reflect their unique needs and circumstances.

Introduction

Close your eyes and envision your dream retirement. Are you strolling along a sandy beach with a delightful book in hand? Or perhaps you’re relishing the joy of finally having the time to dedicate to your cherished hobbies? Now, open your eyes. How confident do you feel about making that dream a reality? If you’re like many women, retirement planning can seem daunting, even elusive. You’re not alone — and it’s not your fault.

From longer lifespans to career breaks, women face unique challenges when it comes to planning for those golden years. Couple that with the ever-present gender wage gap, and it’s no wonder that financial security in retirement can feel like an uphill battle. But fret not. With the right strategies, navigating this complex landscape can become a journey of empowerment and confidence-building.

1. Understanding the Retirement Landscape for Women

Imagine walking a mile with a backpack. Not too hard, right? Now picture adding a few extra pounds to that bag every few steps. Feels a little heavier, doesn’t it? By the end of the mile, you’re likely to feel the strain, and finishing the journey becomes all the more challenging.

This is the predicament many women find themselves in when navigating the path to retirement. The “extra weight” comes in the form of unique challenges that can make planning for a secure future feel more burdensome. But don’t worry, with understanding and smart strategies, you can get through that journey with less strain and more assurance. So what are these challenges, and how can they impact your retirement planning? Let’s dive in.

A. The Gender Wage Gap and Its Impact on Retirement Savings

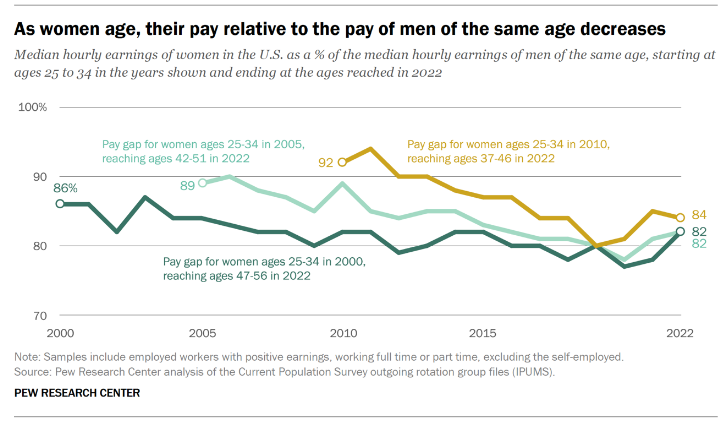

Did you know that as of 2020, women in the US still earn only 82 cents for every dollar earned by men? That’s like paying full price for a product and only receiving 82% of it! This wage gap can significantly affect your ability to accumulate retirement savings over time. Lower earnings mean less disposable income to put away for retirement and less to contribute to social security, affecting your benefits in the long run.

Figure Legend: Data show that women aged 25–34 have neared wage equality with men since 2007, earning around 90 cents to the dollar. However, as these women age, the wage gap widens. For instance, women in this age group in 2010 earned 92% of what their male counterparts did, but by 2022, only 84%. This trend persists.

B. Longer Life Expectancies: A Blessing and a Challenge

Here’s an interesting paradox: women tend to live longer than men — about five years more on average. Now, while a longer life is a blessing, it also means your retirement savings need to stretch further. And this reality brings up the question — are you prepared for this longevity?

C. Career Interruptions: How They Affect Retirement Planning

Ask any woman about juggling career and family, and she’ll likely have a story to share. From maternity leaves to caring for elderly parents, women often have to take career breaks. These interruptions can mean periods without income or reduced contributions to retirement funds, ultimately leading to lower retirement savings.

Understanding these challenges is the first step to overcoming them. Like any journey, the path to a secure retirement isn’t always easy, and the unique hurdles that women face can make it even tougher. But by recognizing these hurdles, you’re already halfway through tackling them.

2. Key Concerns for Women in Retirement Planning

“Have you ever tried solving a puzzle without having all the pieces? It can be quite frustrating, right? Now, what if we told you that retirement planning for many women feels like just that — a puzzle with missing pieces? While it can feel overwhelming, the good news is that with knowledge and planning, you can find those missing pieces and see the whole picture. Let’s explore some of the key concerns you might face.

A. Outliving Savings: The Fear of Many Women

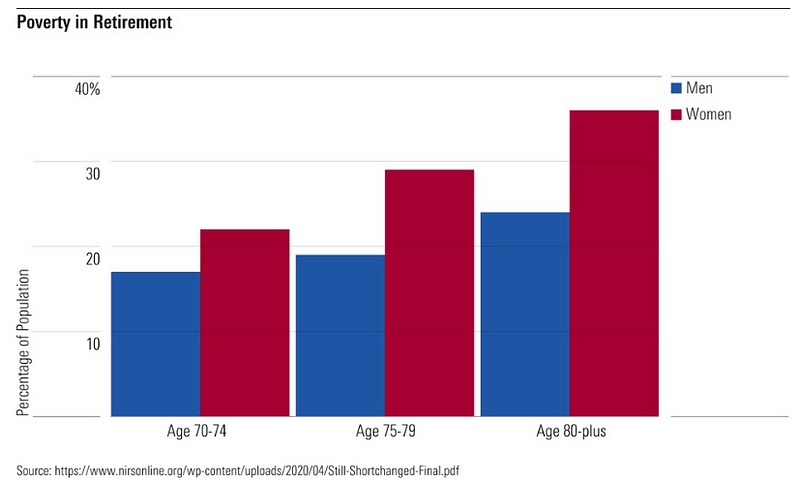

The fear of outliving savings haunts many women. It’s akin to trying to reach a destination with just enough fuel, but with no fuel stations in sight. According to an article on Investopedia, this fear is accentuated for women due to factors like longer lifespans, career breaks, and the wage gap. But with strategic financial planning involving diverse income streams, we can overcome this fear.

Figure Legend: Percentage of women facing financial crisis in retirement is higher than men.

B. Medical Expenses in Retirement: A Rising Concern

Let’s talk about the elephant in the room — the skyrocketing medical expenses. It’s like the ticking health time bomb, waiting to deplete your hard-earned retirement funds. A report by Fidelity indicates that an average retired couple age 65 in 2021 may need approximately $300,000 saved (after tax) to cover health care expenses in retirement. With women living longer, their healthcare costs are bound to be higher.

How can we defuse this ticking time bomb? By considering a Health Savings Account or factoring healthcare costs into our retirement savings plan. And remember, prevention is better than cure; an active, healthy lifestyle can help reduce future medical costs.

C. The Financial Implications of Widowhood

The death of a spouse can be a significant emotional blow. But did you know it can also deliver a financial one? Many women face a decrease in income when they lose their partner, which can dramatically affect their financial security. In fact, the poverty rate for widowed women aged 65 or older is three times that of their married counterparts. It’s a sobering thought, but one that needs to be considered when planning for retirement.

As you can see, retirement planning for women isn’t a one-size-fits-all affair. It’s an intricate puzzle that needs to be solved with careful planning and strategy.

3. Retirement Savings Options: Making the Most of What You Have

Let’s imagine retirement as a mountain peak, and your current financial situation as base camp. Between you and the summit lies an arduous climb, dotted with potential stumbling blocks. But, with the right equipment (read: savings options), this climb can become a fulfilling journey. So, let’s gear up!

A. Making the Most of Employer-Sponsored Retirement Plans

Think of your employer-sponsored retirement plan like your climbing guide. It’s there to help you, and ignoring it is akin to dismissing the advice of an experienced sherpa. These plans, whether 401(k)s or 403(b)s, are a major boon for many reasons. Firstly, the tax benefits — contributions lower your taxable income, and your earnings grow tax-free. Sounds great, right?

Moreover, many employers provide a matching contribution. Let’s break it down. Say your employer matches 50% of your contributions up to 6% of your salary. If you earn $60,000 and contribute $3,600 (6% of your salary), your employer would add another $1,800. That’s free money! Who would want to turn that down?

According to a report from the Bureau of Labor Statistics, in 2020, about 55% of civilian workers had access to a retirement plan at work. If you’re part of the remaining percentage not taking advantage of this benefit, isn’t it time you reconsidered?

B. Individual Retirement Accounts (IRAs): A Must-Have for Women

Next, we have the trusty IRA, akin to your climbing boots. It’s not as noticeable as the guide, but it’s vital for a successful ascent. IRAs come in two forms — Traditional and Roth — each offering unique tax advantages.

Traditional IRAs can provide a tax deduction when you contribute, while Roth IRAs allow for tax-free withdrawals in retirement. However, eligibility for these benefits depends on your income and participation in an employer plan.

According to the IRS, the contribution limit for 2023 is $6,000, or $7,000 if you’re aged 50 or older. This highlights how IRAs help you march ahead in your retirement journey.

C. Using Health Savings Accounts (HSAs) to Plan for Medical Costs

Finally, we have the Health Savings Account (HSA) — your first-aid kit. Just like you shouldn’t ignore health risks while climbing, you can’t overlook the potential for increased medical costs in retirement.

An HSA is a unique tool that lets you contribute, grow, and withdraw funds tax-free for qualified medical expenses. What’s more, according to HealthCare.gov, the unspent money rolls over year after year.

Remember, the climb to a comfortable retirement isn’t easy. But with these saving options at your disposal, you can transform it from an uphill battle into a steady, achievable hike.

4. The Role of Insurance in Women’s Retirement Planning

“Ever tried walking a tightrope without a safety net beneath? It’s scary, isn’t it? Now think about your retirement planning. Insurance is like that safety net, providing financial protection and peace of mind for your retirement journey. So let’s explore how different types of insurance can bolster your retirement plans.

A. Understanding the Different Types of Insurance

Imagine a toolbox. Each tool has a specific purpose, right? Similarly, different types of insurance serve specific needs in your retirement planning. From life insurance to long-term care insurance, each policy has its role in securing your financial future. The trick lies in understanding what each tool does and when to use it.

B. When to Consider Long-Term Care Insurance

Picture long-term care insurance as a trusted caretaker, ready to step in when you need it most. This type of insurance covers services that regular health insurance may not, like assistance with daily activities due to chronic illness or disability. Women, living longer, are more likely to require long-term care at some point. So, doesn’t it make sense to have a plan in place to cover these potential costs?

C. The Place for Life Insurance in Retirement Planning

Life insurance is like a faithful steward, carrying out your last wishes and providing for your loved ones when you’re no longer around. Apart from providing death benefits, certain policies, like whole life or indexed universal life, can also serve as a source of tax-advantaged income during retirement. So, ask yourself this — is your financial legacy secure?

Incorporating insurance into your retirement planning is like building a financial safety net. It may not be the most glamorous part of the process, but it’s certainly an important one. Because when it comes to ensuring a secure retirement, it’s always better to be safe than sorry.

5. Estate Planning: Preserving Your Wealth and Legacy

Are you a master juggler, expertly balancing career, family, and personal commitments? That’s great! But have you forgotten about the one ball that’s easy to drop and hard to pick up again? That’s right, we’re talking about estate planning.

Consider this: When you leave this world, your wealth and possessions don’t accompany you. What happens to them? They are your legacy, your final love letter to the people and causes you care about. But without a well-crafted plan, your wishes could end up as just that — wishes.

A. Wills, Trusts, and Estates: What Women Need to Know

Have you ever tried assembling a flat-pack furniture piece without instructions? Frustrating, isn’t it? Wills, trusts, and estates can seem like that — daunting, complex, and full of legalese. But they’re the instructions you leave behind, ensuring your wealth goes exactly where you want it to.

A will, the cornerstone of estate planning, outlines who will inherit your assets and when. According to AARP, a shocking 60% of American adults don’t have a will. If you’re in that number, it’s time for a change.

Trusts, on the other hand, are like VIP passes for your assets, allowing them to bypass the public and often lengthy probate process. And estates? That’s just a fancy term for everything you own.

B. The Importance of Powers of Attorney and Living Wills

In life, we often appoint someone to ‘hold the fort’ when we can’t. This is essentially what powers of attorney and living wills do. A power of attorney appoints someone to make financial or health decisions on your behalf if you’re unable to do so. A living will outlines your healthcare wishes if you become seriously ill and can’t express your wishes yourself. Seems pretty crucial, doesn’t it?

According to the National Institute on Aging, everyone needs these legal documents, irrespective of their age or health status.

Remember, it’s not about courting morbidity; it’s about taking control, leaving no room for ambiguity, and making a challenging time slightly less so for your loved ones.

Estate planning may seem like a daunting task, but it’s your legacy we’re talking about — a reflection of your life, your values, and your love. Are you ready to preserve it?

6. Building Your Retirement Income Stream: Annuities and Beyond

Is it possible to enjoy a retirement that isn’t marred by constant worries about money? Can you look at your golden years with anticipation rather than anxiety? Yes, absolutely! With the right planning and strategic moves, retirement can be the best chapter of your life. Let’s dive into the world of annuities and beyond, creating an income stream that flows long into your retirement years.

A. The Benefits of Annuities for Women

Imagine a paycheck arriving at your door every month for the rest of your life, come rain or shine. Sounds too good to be true, right? That’s the power of an annuity. In its simplest form, an annuity is a contract with an insurance company that promises to pay you a steady income in exchange for a lump sum or regular contributions. With women’s longer average life expectancy, annuities can be a potent tool to ensure financial stability and fight the specter of outliving one’s savings.

According to the American Council of Life Insurers, annuities are a favorite among women for retirement income planning. They act as a safety net, catching you even when the market tumbles. Are they right for you? That’s a question best answered with a financial advisor who understands your unique situation.

B. Social Security Strategies for Women

Social Security is an essential piece of the retirement puzzle. But how and when to claim it can seem like trying to solve a Rubik’s Cube. According to the Social Security Administration, delaying benefits until after your full retirement age (FRA) can increase your monthly payment by as much as 8% per year until age 70. Given the longevity advantage that women have, delaying Social Security could pay off handsomely over a longer retirement.

C. Income Generation from Investments

In the quest for retirement income, the siren call of investments can be hard to resist. And why should you? From bonds and dividend-paying stocks to real estate and mutual funds, there are countless avenues to explore. It’s about creating a well-diversified portfolio, one that can weather market storms and deliver the income you need. As stated in a report by Bloomberg, women tend to be more disciplined investors, a trait that can significantly boost returns over time.

But remember, it’s not just about piling on assets; it’s about structuring them to deliver a steady, reliable income stream. Need some help charting your course? It might be time to consider partnering with a financial advisor who can guide you through these complex decisions.

7. Getting Help: Working with a Financial Advisor

“Have you ever tried to navigate a foreign city without a map or GPS? You might eventually find your way, but there’s a high likelihood of unnecessary detours, dead-ends, and stress. The world of retirement planning can feel much the same. That’s where a financial advisor comes in, acting like your personal GPS guiding you through the intricate streets of retirement planning.

A. The Role of a Financial Advisor in Retirement Planning

Imagine having a personal chef who knows your dietary needs, allergies, and favorite flavors. Just as this chef would craft the perfect meal plan for you, a financial advisor customizes a retirement plan that fits your financial situation, goals, and risk tolerance. A good financial advisor can help you navigate tax strategies, manage investment risks, and adjust your plan as life changes — all crucial ingredients for a secure retirement.

B. How to Choose a Financial Advisor That Understands Women’s Needs

Remember when we talked about a tailor-made dress that fits perfectly? Similarly, you need a financial advisor who understands and addresses the unique financial challenges women face. When choosing an advisor, look for one who takes the time to understand your specific needs, provides personalized advice, and educates you along the journey. After all, isn’t it best when someone ‘gets’ you?

Embarking on the retirement planning journey can seem intimidating, but remember, you don’t have to do it alone. A reliable financial advisor can help make the process less daunting, enabling you to create a retirement plan that is as unique as you are.

Conclusion

The unique challenges that women face in retirement planning might seem daunting, but as we have seen, they can be tackled with knowledge, strategic planning, and professional help.

From understanding the impact of the gender wage gap and longevity risk to choosing the right insurance products and estate planning tools, every step you take today can make a significant difference in your retirement years. It is never too early or too late to start planning for your retirement, but the sooner you begin, the better prepared you will be.

But remember, you are not alone on this journey. A financial advisor can be your trusted partner, guiding you through the labyrinth of retirement planning. A well-informed advisor can help you navigate these challenges, tailored to your unique needs and life circumstances.

Your journey to a secure and fulfilling retirement starts with a single step. So, are you ready to take that step today?

Frequently Asked Questions (FAQ)

How does the gender wage gap impact women’s retirement planning?

The gender wage gap results in lower lifetime earnings for women, which means they often have less money to save for retirement. This can result in smaller nest eggs and lower Social Security benefits since these are calculated based on lifetime earnings. Despite these challenges, women can strategize to build adequate retirement savings through early and aggressive saving, optimizing Social Security benefits, and considering insurance products like long-term care insurance.

How does longevity risk affect women’s retirement planning?

Longevity risk is the risk of outliving your savings. As women typically live longer than men, they need to plan for a longer retirement period. This means women may need to save more to cover their expenses for a longer time and consider the potential need for long-term care.

What types of insurance should women consider in their retirement planning?

Long-term care insurance can be particularly important for women as they often live longer and may require long-term care. Life insurance, including term life, indexed universal life, and whole life policies, can also be beneficial for protecting your income and providing for your heirs.

Why is estate planning important in retirement planning for women?

Estate planning allows women to control how their assets will be distributed after their death. Through wills, trusts, and powers of attorney, women can ensure their wealth is preserved and passed on according to their wishes.

How can a financial advisor help in retirement planning for women?

A financial advisor can provide personalized advice taking into account the unique challenges women face in retirement planning. They can guide you through saving strategies, choosing appropriate insurance products, understanding Social Security benefits, and estate planning. By working with an advisor who understands women’s needs, you can develop a tailored plan to secure your financial future.