Summary:

In this blog post, we explored the benefits and strategies for maximizing retirement savings through tax-deferred plans. We discussed the concept of tax deferral and its significance in allowing investments to grow over time through the power of compounding. By starting early, contributing up to the maximum, and taking advantage of catch-up contributions, individuals can optimize their savings potential. We also highlighted the importance of employer matching programs and offered tips for diversifying investments within tax-deferred plans.

Introduction:

Retirement is a milestone that many of us eagerly anticipate, but it also comes with its fair share of concerns. Will you have enough money to cover your expenses during retirement? How can you navigate the rising costs of medical expenses? And how can you pass on your wealth to your loved ones?

In this article, we’ll shed light on the power of tax-deferred pension and retirement savings plans in bolstering your retirement savings. These plans offer unique advantages that can help you grow your nest egg and achieve financial peace of mind.

1. Understanding Tax-Deferred Pension Plans

A. What are tax-deferred pension plans?

When it comes to securing a comfortable retirement, tax-deferred pension plans are an essential tool in your financial arsenal. These plans provide individuals with a structured and efficient way to save for their golden years while reaping significant tax benefits along the way.

In simple terms, tax-deferred pension plans are retirement savings vehicles that allow you to contribute a portion of your income on a pre-tax basis. This means that the money you invest in these plans is deducted from your taxable income, reducing the amount of income tax you owe in the current year. By deferring taxes until withdrawal, you have the opportunity to grow your retirement savings more efficiently.

B. Examples of popular tax-deferred pension plans

- Traditional 401(k): The traditional 401(k) is one of the most common and well-known tax-deferred pension plans. It allows employees to contribute a portion of their salary on a pre-tax basis, up to certain limits set by the Internal Revenue Service (IRS). Employers may also offer matching contributions, further enhancing the savings potential.

- Individual Retirement Accounts (IRAs): Traditional IRAs are another popular option for tax-deferred retirement savings. With an IRA, individuals can contribute pre-tax dollars, subject to certain income limitations. These plans provide flexibility in investment options and can be opened by individuals independently of their employers.

- 403(b) Plans: Designed for employees of public schools, tax-exempt organizations, and certain ministers, 403(b) plans offer similar tax advantages as 401(k) plans. These plans allow employees to contribute a portion of their income on a pre-tax basis and may include employer matching contributions.

C. Key features and advantages of tax-deferred pension plans

- Tax Savings: One of the primary benefits of tax-deferred pension plans is the potential tax savings they offer. By contributing pre-tax dollars, you effectively lower your taxable income, which can lead to substantial savings when it comes time to file your annual tax return. This reduction in taxes allows you to keep more of your hard-earned money in your pocket, giving you additional funds to invest and grow over time.

- Compound Growth: Another advantage of tax-deferred pension plans is the power of compound growth. The contributions you make to these plans, along with any earnings generated, have the opportunity to grow exponentially over the years. Since taxes are deferred until withdrawal, the money that would have otherwise been paid in taxes remains invested, compounding over time and accelerating the growth of your retirement savings.

- Employer Contributions: Many tax-deferred pension plans, such as 401(k) plans, offer the added benefit of employer contributions. Employers may match a percentage of your contributions, effectively providing you with free money that goes directly into your retirement savings. This employer match can significantly boost the growth of your retirement nest egg and help you reach your goals faster.

- Simplified Employee Pension (SEP) IRAs: Designed for self-employed individuals and small business owners, SEP IRAs allow for higher contribution limits and potential tax deductions.

2. Exploring Retirement Savings Plans

A. Overview of retirement savings plans

Retirement savings plans offer individuals the opportunity to set aside funds specifically dedicated to their future financial security. Let’s take a closer look at the benefits and features of these plans, helping you make informed decisions to secure a comfortable retirement.

Retirement savings plans, also known as retirement accounts, are financial tools designed to help you accumulate and grow your retirement funds. These plans provide a dedicated space for your savings, allowing them to grow over time through investments and taking advantage of potential tax benefits. By proactively setting money aside in a retirement savings plan, you can ensure a stable and rewarding retirement.

B. Types of retirement savings plans available

There are several types of retirement savings plans available, each with its unique features and advantages. Let’s explore some of the most common options:

- 401(k) Plans: The 401(k) plan is a popular employer-sponsored retirement savings plan that allows employees to contribute a portion of their salary before taxes. Employers may also offer matching contributions, which can significantly boost your savings. These plans often offer a range of investment options, giving you the flexibility to choose the best strategy for your retirement goals.

- Individual Retirement Accounts (IRAs): IRAs are personal retirement savings accounts that individuals can open independently. Traditional IRAs allow for tax-deductible contributions, providing immediate tax benefits. Roth IRAs, on the other hand, are funded with after-tax dollars, but withdrawals in retirement are typically tax-free. IRAs offer a wide range of investment options, including stocks, bonds, mutual funds, and more.

- SEP-IRAs and SIMPLE IRAs: These retirement savings plans are tailored for self-employed individuals and small business owners. SEP-IRAs (Simplified Employee Pension IRAs) and SIMPLE IRAs (Savings Incentive Match Plan for Employees) provide tax advantages and straightforward contribution rules. These plans offer flexibility in contribution amounts and can be an excellent choice for entrepreneurs seeking retirement savings options.

C. Comparative analysis of different retirement savings plans

Comparing different retirement savings plans is essential to find the best fit for your individual circumstances. Here’s a brief comparative analysis of some key factors:

- Contribution Limits: Each retirement savings plan has specific contribution limits imposed by the IRS. Understanding these limits helps you determine how much you can contribute annually, maximizing your retirement savings potential.

- Tax Advantages: Different plans offer varying tax benefits. Traditional 401(k)s and traditional IRAs provide upfront tax advantages, as contributions are made with pre-tax dollars. Roth IRAs and Roth 401(k)s, on the other hand, offer tax-free qualified withdrawals in retirement. Evaluating the tax advantages can help you choose the plan that aligns with your tax situation and long-term goals.

- Employer Contributions: Employer matching contributions can significantly impact the growth of your retirement savings. Many 401(k) plans include employer matches, while IRAs do not. Considering the availability of employer contributions is important when evaluating the benefits of each plan.

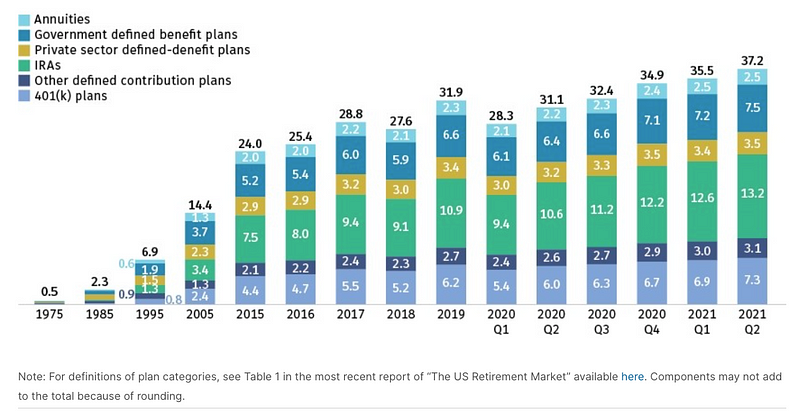

Figure Legend: By March 31, 2021, assets in all retirement plans accounts to a total of $37.2 trillion.

3. The Power of Tax Deferral in Retirement Savings

A. Tax deferral and its significance

Tax deferral refers to the strategy of delaying the payment of taxes on investment earnings until a later date, typically during retirement. By utilizing tax-deferred retirement savings plans, individuals can take advantage of the power of compounding and potentially reduce their tax burden over time.

The significance of tax deferral lies in its ability to maximize the growth potential of your retirement savings. Instead of paying taxes on investment gains annually, tax-deferred plans allow you to reinvest those earnings, compounding them over time. This compounding effect can lead to significant growth in your retirement nest egg.

B. How tax deferral impacts retirement savings growth

Tax deferral plays a crucial role in accelerating the growth of your retirement savings. Here’s how it works:

- Compounding Growth: When you contribute to a tax-deferred retirement savings plan, your investments have the opportunity to grow exponentially. By deferring taxes on your contributions and any earnings, the money that would have gone towards taxes remains invested, compounding over time. The longer you can keep your investments growing tax-free, the more substantial the impact on your retirement savings.

- Increased Investment Potential: Tax deferral allows you to invest a larger portion of your income upfront, as you’re not immediately deducting taxes. By contributing pre-tax dollars, you have more funds available to invest. This increased investment potential, coupled with the compounding effect, can significantly boost the overall growth of your retirement savings.

- Lower Tax Bracket in Retirement: Another advantage of tax deferral is the potential to be in a lower tax bracket during retirement. Many individuals find themselves in a lower tax bracket once they stop working and rely on their retirement savings as their primary source of income. This means that when you withdraw funds from your tax-deferred retirement accounts, you may pay less in taxes compared to when you were actively employed.

C. Case studies illustrating the benefits of tax-deferred savings

To better understand the benefits of tax-deferred savings, let’s consider a couple of case studies:

- Sarah and John: Sarah and John are a couple in their early 40s, diligently saving for retirement. They contribute $10,000 annually to their tax-deferred retirement accounts for 25 years. Assuming an average annual return of 7%, their investment grows to over $615,000. By deferring taxes until withdrawal, they maximize their savings potential and achieve significant growth.

- Mike: Mike, a 30-year-old professional, decides to contribute $5,000 annually to his tax-deferred retirement account for 35 years. With an average annual return of 8%, his investment grows to nearly $840,000. The power of compounding, coupled with tax deferral, allows Mike to build a substantial retirement fund.

These case studies highlight the long-term benefits of tax-deferred savings. By taking advantage of tax deferral, individuals have the potential to accumulate significant wealth over time, providing financial security and peace of mind in retirement.

4. Maximizing Your Retirement Savings with Tax-Deferred Plans

A. Strategies for optimizing contributions to tax-deferred plans

When it comes to saving for retirement, maximizing your contributions to tax-deferred plans is key to building a substantial nest egg. Here are some strategies to help you make the most of these retirement savings vehicles:

- Start Early: The power of compounding works best when you have time on your side. By starting to contribute to tax-deferred plans as early as possible, you allow your investments to grow over a more extended period. Even small contributions in your early years can have a significant impact due to the compounding effect.

- Contribute up to the Maximum: Each tax-deferred plan has contribution limits set by the IRS. To optimize your savings, strive to contribute the maximum allowed amount. For example, if you have a 401(k) plan, contribute the maximum limit, taking advantage of the tax benefits and potential employer matches.

- Take Advantage of Catch-Up Contributions: If you’re over 50 years old, you’re eligible for catch-up contributions in most retirement savings plans. These additional contributions allow you to boost your savings potential and make up for any earlier years with lower contributions. Take advantage of this opportunity to accelerate your retirement savings.

B. Leveraging employer-matching programs for enhanced savings

One of the most powerful tools for maximizing your retirement savings is employer matching programs. Here’s how you can leverage them:

- Contribute at Least the Employer Match: If your employer offers a matching contribution, make sure to contribute at least the amount required to receive the full match. Employer matches are essentially free money that goes directly into your retirement savings. Failing to contribute the required amount means leaving money on the table.

- Increase Contributions with Salary Raises: Whenever you receive a salary increase or bonus, consider increasing your contributions to take full advantage of the matching program. By doing so, you not only maximize your savings but also enjoy the benefits of compounding on the additional funds.

- Understand Vesting Schedules: Some employer matches may be subject to vesting schedules, meaning you need to work for a certain period before the matching funds become fully yours. Be aware of the vesting schedule and factor it into your long-term retirement savings strategy.

C. Tips for diversifying investments within tax-deferred plans

Diversifying your investments within tax-deferred plans is essential to manage risk and maximize potential returns. Here are a few tips to consider:

- Allocate Across Asset Classes: Spread your investments across different asset classes, such as stocks, bonds, and real estate investment trusts (REITs). Diversifying your portfolio helps reduce the impact of any single investment performing poorly and enhances your chances of capturing growth opportunities.

- Consider Target-Date Funds: Target-date funds are investment vehicles that automatically adjust their asset allocation based on your expected retirement date. These funds provide diversification and gradually shift towards a more conservative approach as you approach retirement. They can be a convenient option for individuals who prefer a hands-off approach to investing.

- Regularly Review and Rebalance: Regularly review your investment portfolio within tax-deferred plans to ensure it aligns with your risk tolerance and retirement goals. Rebalance your portfolio periodically to maintain the desired asset allocation. Market fluctuations may cause your portfolio to drift away from the intended balance, and rebalancing helps realign it.

5. Addressing Concerns and Common Questions

A. Potential drawbacks or limitations of tax-deferred plans

While tax-deferred retirement savings plans offer numerous advantages, it’s essential to be aware of potential drawbacks and limitations. Here are a few considerations:

- Contribution Limits: Tax-deferred plans have annual contribution limits set by the IRS. Depending on your income and plan type, there may be restrictions on how much you can contribute each year. It’s important to be mindful of these limits to ensure you’re optimizing your savings potential.

- Early Withdrawal Penalties: Most tax-deferred plans impose penalties for withdrawing funds before reaching a certain age, typically 59½. Withdrawing money early may result in additional taxes and penalties, eroding your savings. It’s crucial to have a solid understanding of the withdrawal rules and plan accordingly to avoid unnecessary penalties.

- Required Minimum Distributions (RMDs): Once you reach a certain age, usually 72 for traditional IRAs and 401(k)s, you’re required to start taking minimum distributions from your tax-deferred accounts. These distributions are subject to taxation and can impact your overall retirement income strategy. Failing to take RMDs can result in significant penalties, so it’s important to factor them into your financial planning.

B. Addressing concerns about access to funds and withdrawal penalties

Access to funds and potential withdrawal penalties are valid concerns for many individuals. Here’s how you can navigate these concerns:

- Emergency Fund: To address the concern of needing immediate access to funds, it’s important to maintain an emergency fund outside of your tax-deferred retirement accounts. This fund acts as a safety net, providing you with readily available cash for unexpected expenses. By having a dedicated emergency fund, you can avoid tapping into your retirement savings prematurely.

- Explore Loan Options: Some tax-deferred plans, such as 401(k)s, may allow you to take out loans against your account balance. While it’s generally advisable to avoid borrowing from your retirement savings, these loan options can provide a solution if you find yourself in a financial bind. However, it’s crucial to consider the potential impact on your long-term savings goals and the repayment terms before taking a loan.

- Plan for Withdrawals: Careful planning can help minimize the risk of withdrawal penalties. By mapping out your retirement income needs and creating a withdrawal strategy, you can ensure a smooth transition from saving to spending. Consider working with a financial advisor to develop a comprehensive retirement income plan that aligns with your goals and minimizes unnecessary penalties.

C. How to choose the right tax-deferred plan based on individual needs

Choosing the right tax-deferred plan depends on your individual circumstances and goals. Consider the following factors when making your decision:

- Employer-Sponsored Plans: If your employer offers a retirement savings plan with an employer match, such as a 401(k), start by contributing enough to receive the full match. Taking advantage of employer contributions is like receiving free money, boosting your savings potential.

- Individual Retirement Accounts (IRAs): If you’re self-employed or your employer doesn’t offer a retirement plan, consider opening an IRA. Traditional IRAs provide tax-deductible contributions, while Roth IRAs offer tax-free withdrawals in retirement. Evaluate your current and future tax situation to determine the most beneficial option.

- Seek Professional Advice: Choosing the right tax-deferred plan can be complex. Seeking guidance from a qualified financial advisor can help you navigate the various options and select the plan that aligns best with your financial goals, risk tolerance, and individual needs.

By considering potential drawbacks, addressing concerns about access to funds, and choosing the right plan based on your needs, you can maximize the benefits of tax-deferred retirement savings.

Conclusion:

In conclusion, planning for a secure retirement requires careful consideration of various factors, including maximizing Social Security benefits, navigating federal taxes, and capitalizing on tax breaks. By understanding the ins and outs of retirement planning, you can take proactive steps to build a solid financial foundation for your future.

First and foremost, Social Security benefits play a crucial role in retirement income. By strategizing when and how to claim these benefits, you can optimize your monthly payments and potentially enhance your overall retirement financial security. Take the time to explore claiming strategies, coordinate spousal benefits, and consider delaying benefits to maximize your Social Security retirement benefit.

Federal taxes are another aspect that shouldn’t be overlooked. Understanding the tax implications of your retirement income and leveraging available tax breaks can significantly impact your post-retirement financial picture. Explore deductions, credits, and tax planning strategies to minimize your tax liabilities and retain more of your hard-earned money for your retirement needs.

While planning for retirement can be complex, seeking professional advice and legal support can provide invaluable guidance. Consult with financial advisors, tax experts, and attorneys who specialize in retirement planning and can help you navigate the intricacies of Social Security, federal taxes, and legal considerations.

Frequently Asked Questions (FAQ)

What are the potential drawbacks of tax-deferred retirement plans?

While tax-deferred retirement plans offer numerous benefits, they also have limitations. Some potential drawbacks include contribution limits set by the IRS, early withdrawal penalties, and required minimum distributions (RMDs) once you reach a certain age. It’s important to be aware of these factors and plan accordingly.

How can I access funds in tax-deferred retirement accounts without penalties?

While accessing funds in tax-deferred retirement accounts before reaching the eligible age can result in penalties, there are strategies to mitigate this. Building an emergency fund outside of retirement accounts can provide immediate access to funds for unexpected expenses. Additionally, some plans allow loans against the account balance, although borrowing from retirement savings should be approached with caution.

How do I choose the right tax-deferred plan for my needs?

Choosing the right tax-deferred plan depends on your individual circumstances and goals. If your employer offers a retirement plan with matching contributions, start by contributing enough to receive the full match. Consider factors such as eligibility, contribution limits, and potential tax advantages when selecting between employer-sponsored plans or individual retirement accounts (IRAs). Consulting with a financial advisor can provide personalized guidance.

What role does Social Security play in retirement planning?

Social Security benefits can provide a significant portion of retirement income. Understanding how benefits are calculated, considering factors such as life expectancy and spousal benefits, and strategizing when to claim benefits can help maximize Social Security payments. It’s important to incorporate Social Security into your overall retirement plan and consider the long-term impact on your financial security.

How does tax deferral benefit retirement savings?

Tax deferral allows individuals to delay paying taxes on their investment earnings until they withdraw the funds during retirement. By deferring taxes, the money that would have gone towards taxes remains invested, compounding over time and potentially resulting in significant growth in retirement savings.