Summary:

In the ever-evolving world of finance, understanding annuities — essentially a series of payments — becomes paramount. The blog dives deep into the intricacies of the Present Value of an Ordinary Annuity Table, highlighting its significance in modern finance. Through interactive tools like dynamic spreadsheets and annuity calculators, readers are empowered to grasp complex concepts, from the time value of money to the role of annuity tables. The digital age brings forth interactive annuity tables, offering real-time insights and transforming the way we view future annuity payments. With a focus on making informed decisions, the blog emphasizes the importance of financial literacy in today’s landscape.

Introduction

In the dynamic world of finance, have you ever pondered the true worth of your future cash flows? Enter the Present Value of an Ordinary Annuity Table (pv annuity table) — a game-changer in understanding the current value of a series of future payments. Whether you’re an investor eyeing the next big opportunity, evaluating loan options, or meticulously planning for a comfortable retirement, this table is your compass. It’s not just a set of numbers; it’s a tool that empowers you to make informed financial decisions in an ever-evolving economic landscape. Dive in with us as we unravel the intricacies of this essential tool and illuminate its pivotal role in modern finance.

1. Understanding Annuities

A. Definition and Basics

What is an annuity?

An annuity is essentially an insurance contract that promises future income payments in exchange for present contributions. These contracts are sold by financial institutions, primarily to bolster retirement plans. They can be a valuable tool for those looking to secure their financial future. Annuities can be structured in various ways, offering different features and benefits. The primary goal, however, remains consistent: to provide a predictable income stream, especially during retirement years.

Differentiating between ordinary annuities and annuities due.

There are several types of annuities, including fixed, variable, and indexed. A fixed annuity guarantees a specific rate of return and payout, making it a safer option for those who prefer predictability.

Variable annuities, on the other hand, offer returns based on the performance of chosen investment options, introducing a higher risk-reward scenario.

Indexed annuities combine features of both, linking returns to a market index while also offering a minimum guaranteed interest rate.

B. Key Features and Advantages

Guaranteed income for retirement.

One of the standout features of annuities is the guaranteed income they provide. Especially for retirees, this can be a game-changer. With the right annuity, you can ensure a steady cash flow during your golden years, irrespective of market fluctuations or economic downturns.

Offset risks of outliving your money.

The fear of outliving one’s savings is real, especially given the increasing life expectancies. Annuities address this concern head-on. By offering a fixed income stream, often for life, they ensure that you won’t run out of funds even if you live longer than anticipated.

Predictable and steady income streams.

Regardless of the type of annuity you choose, the primary benefit remains consistent: predictable payments. Whether these payments are guaranteed for a set period or for life, they offer peace of mind. This predictability can be especially comforting in an unpredictable economic landscape, making annuities a favored choice for many looking to secure their financial futures.

2. The Time Value of Money: A Pillar of Financial Wisdom

A. Definition and Importance

Why Money Today is Worth More Than Tomorrow: Imagine you’re offered $100 today or the same amount a year from now. Which would you choose? Most would opt for the money now. This isn’t just impatience; it’s a financial principle known as the Time Value of Money (TVM). At its core, TVM acknowledges that a dollar in hand today holds more value than the promise of a dollar in the future. This is due to its potential earning capacity.

In essence, the Time Value of Money is more than just a financial concept; it’s a lens through which we view our financial decisions, ensuring we’re always one step ahead.

3. Present Value of an Ordinary Annuity (pv annuity table): Dive Deep

A. The Concept Explained

How it differs from future value.

Money today is worth more than the same amount in the future due to its potential earning capacity. This is where the difference between present value and future value comes into play. While future value tells you what an investment will be worth in the future, present value reveals what a future sum of money is worth today.

The role of discount rates in determining present value.

Think of discount rates as the “time machine” of finance. They help us travel between the present and the future, determining the current worth of future cash flows. A higher discount rate reduces the present value, reflecting the idea that future money is less valuable. It’s like the interest rate in reverse; instead of growing your money, it discounts future amounts back to their value today.

B. Calculating Present Value (pv annuity table)

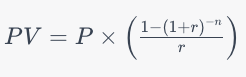

Introducing the formula.

To calculate the present value of an ordinary annuity, use the formula:

Where:

- PV is the present value.

- P is the payment amount per period.

- r is the interest rate per period.

- n is the number of payments.

Factors affecting the calculation: interest rate, number of payments, and type of annuity.

The interest rate plays a pivotal role; a higher rate reduces the present value. The number of payments impacts how many times you’ll receive the annuity, and the type of annuity (ordinary or due) determines when these payments occur.

C. Practical Uses of the Present Value Formula

Comparing options for keeping or selling your annuity.

Let’s say you’re offered a lump sum in exchange for your annuity payments. Using the present value formula, you can determine the current worth of those future payments, helping you decide whether the offer is fair.

Making informed financial decisions.

Understanding the present value of an annuity empowers you to make informed decisions, whether it’s evaluating investment opportunities, planning for retirement, or assessing loan offers. By grasping this concept, you’re better equipped to navigate the financial seas with confidence.

4. The Essential Role of Annuity Tables

A. What is an Annuity Table?

An annuity table is a financial tool that simplifies the process of determining the future value or present value of an annuity. Picture this: Sarah, a 30-year-old professional, wants to invest in an annuity that promises consistent returns. But how does she determine its worth over time? Enter the annuity table.

Breaking down the components, an annuity table typically consists of:

- Number of periods: This represents the total time frame of the annuity, often in years. For Sarah, if she’s looking at a 20-year annuity, this would be her number of periods.

- Interest rate: This is the rate at which the annuity grows. If Sarah’s annuity offers a 5% annual return, this is her interest rate.

- Factor: This is a multiplier derived from the number of periods and interest rate. It’s the magic number that, when multiplied with the annuity payment, gives the future or present value.

B. How to Use Annuity Tables

Using an annuity table might seem daunting, but it’s simpler than you think. Let’s journey with Sarah as she navigates her annuity table:

- Identify the Interest Rate and Number of Periods: Sarah spots her 5% interest rate and 20-year period on the table.

- Locate the Factor: She then finds the intersection of her interest rate and number of periods. This gives her the factor.

- Calculate: Sarah multiplies her annual annuity payment with the factor to get her future value.

Real-life example: Imagine Sarah invests $1000 annually at a 5% interest rate for 20 years. If her factor is 33.066, her future value would be $33,066 (1000 x 33.066).

Annuity tables, with their structured layout and comprehensive data, are invaluable for financial planning. They bridge the gap between complex calculations and practical decision-making, ensuring that individuals like Sarah can make informed choices about their financial future.

5. Making the Most of Your Annuity: Tips and Tricks

A. Selling Your Annuity

- Factors to Consider: Before selling your annuity, it’s crucial to understand its present value, the future payments you’re entitled to, and the current market conditions. Annuities can offer a steady stream of income, but sometimes, a lump sum might be more beneficial depending on your financial needs.

- Ensuring a Fair Deal: Always consult with a financial advisor or an annuity expert before making a decision. They can provide a comprehensive analysis, ensuring you get a deal that’s in your best interest.

B. Investing in Annuities

- Why Annuities are a Good Financial Product: Annuities can provide guaranteed lifetime income, a feature not commonly found in other investment products. Especially in uncertain economic times, the stability and security offered by annuities become even more attractive.

6. Interactive Element: Dive into the Interactive Annuity Table

A. The Power of Interactivity in Finance

Today, interactive tools are revolutionizing our understanding of complex financial concepts. Why? Because they allow us to experience the data, rather than just read it.

Imagine trying to understand the intricacies of annuities through a static table. It’s like trying to understand the beauty of a painting by reading about it. Interactive tools, on the other hand, let you “touch” and “feel” the data, making the abstract tangible. This shift from static tables to dynamic calculators in the digital age is not just a trend; it’s a necessity for the modern investor.

B. Introducing the Interactive Annuity Table

Enter the Interactive Annuity Table — a game-changer in the world of finance. Unlike traditional tables that remain fixed, this dynamic tool adjusts in real-time based on the data you input. Think of it as a living, breathing entity that responds to your every move. The beauty of real-time calculations is that they provide immediate feedback, allowing you to see the impact of your decisions instantly.

So, how does this differ from traditional tables? Traditional tables give you a snapshot — a moment frozen in time. The Interactive Annuity Table, however, is like a flowing river, constantly adapting and providing fresh insights.

C. How to Use the Interactive Annuity Table

Using the Interactive Annuity Table is a breeze. Start by inputting your desired data — whether it’s the initial investment, interest rate, or time period. As you adjust these variables, watch as the table recalculates before your eyes. To interpret the results, simply look at the projected annuity payments and total returns.

A pro tip? Always double-check your inputs. The more accurate your data, the more reliable the results. And remember, this tool is designed to empower you, giving you the insights you need to make informed decisions.

D. Benefits of the Interactive Approach

The benefits of the interactive approach are manifold. Firstly, it demystifies complex financial concepts, making them accessible to everyone. No longer do you need a finance degree to understand annuities. With the Interactive Annuity Table, you gain an immediate understanding, empowering you to make decisions with confidence.

Moreover, this approach fosters a sense of ownership. You’re not just a passive observer; you’re an active participant, shaping your financial destiny with each input and adjustment.

Conclusion

In the vast ocean of financial planning, understanding the concept of annuities — essentially a series of payments — can be your guiding star. From breaking down the cost equation to utilizing tools like the annuity calculator, we’ve journeyed through the intricacies of ensuring a stable financial future. The Annuity period, a crucial component, determines the frequency and duration of your future annuity payments. But remember, in this digital age, you’re not alone. With dynamic tools at your fingertips, like interactive spreadsheets and calculators, you’re empowered to make informed decisions.

Engage with the tools, play around with the numbers, and envision your financial trajectory. And if you found value in this guide, share it. Let’s create a community where financial literacy is not just a goal but a reality. Engage, learn, and prosper.

Frequently Asked Questions (FAQ)

What are the tax implications of annuities?

Annuities have unique tax implications. The earnings from deferred annuities grow tax-free until withdrawal. When you start receiving payments, the portion of the payment that represents your original investment is tax-free, while the portion that represents the earnings is taxed as ordinary income. It’s essential to consult with a tax professional to understand the specific tax implications for your situation.

How do annuities differ from other retirement investment options like 401(k)s or IRAs?

While annuities provide a guaranteed income stream, 401(k)s and IRAs are retirement savings accounts that offer tax advantages. The primary difference lies in the distribution phase. Annuities guarantee a set payment, while 401(k)s and IRAs depend on the account’s investment performance.

Can I lose money if I invest in an annuity?

The risk associated with annuities depends on the type. Fixed annuities guarantee a minimum rate of return, so your principal is protected. However, with variable annuities, the returns are based on market performance, so there’s a potential for both gains and losses.

Are there fees associated with annuities?

Yes, annuities can have various fees, including surrender charges, mortality and expense risk charges, and investment management fees. It’s crucial to understand all associated costs before purchasing an annuity.

Can I pass on my annuity to my heirs?

Yes, if you haven’t annuitized the contract, the annuity can be passed on to your beneficiaries. However, they might be subject to taxes. If the annuity has been annuitized, the distribution options to beneficiaries will depend on the payout option you chose when purchasing the annuity.