Summary:

Enhancing your financial legacy requires strategic planning, especially with tools like the Employee Retirement Income Security Act (ERISA). ERISA plays a critical role in wealth transfer, offering an advantage in terms of inheritance tax, protecting your heirs from financial burdens. Real-world case studies show the effectiveness of ERISA in retirement planning, illuminating both its success stories and pitfalls. The key to optimization lies in expert tips and seeking professional help for comprehensive ERISA planning.

One of the most crucial elements in this process is understanding the ERISA Beneficiary Designation Form. As a plan participant, your primary and contingent beneficiaries should be clearly defined on this form. Clear communication with your plan sponsor also plays a vital role, ensuring your employee benefit plan aligns with your retirement goals.

Balancing fiduciary requirements and duties within your ERISA-covered retirement plans guarantees the rights and benefits of plan participants. Finally, knowing what happens at the time of death is crucial. Proper designation of primary and contingent beneficiaries, understanding the process of claiming death benefits under ERISA, and ensuring a seamless transfer of benefits are integral steps towards securing a lasting financial legacy for your loved ones.

Introduction

Imagine a financial safety net, woven with the threads of legal safeguards, protecting your retirement nest egg and your beneficiary’s future. That’s ERISA — the Employee Retirement Income Security Act — at work. But what exactly is this powerful piece of legislation, and how does it impact your retirement and wealth transfer plans? Whether you’re a retiree, a soon-to-be retiree, or a financial planner, understanding the importance of ERISA for your retirement plan beneficiary designation is crucial in the realm of retirement planning.

ERISA, a federal law enacted in 1974, was designed to protect the retirement assets of employees. This groundbreaking legislation regulates the majority of private-sector retirement plans, from pensions to 401(k)s, setting minimum standards for participation, vesting, benefit accrual, and funding. The primary aim? To safeguard the retirement income of Americans.

In today’s volatile financial landscape, uncertainty is the only certainty. An ERISA-covered retirement plan becomes your ally in these unpredictable times, especially when it comes to securing the future of your designated beneficiaries. This blog post is a comprehensive guide to navigating the intricate world of ERISA, its role in retirement planning, and its undeniable significance for your retirement plan beneficiary.

1. Understanding ERISA: Its Role in Retirement Planning

A. The Impact of ERISA on Retirement Plans

Navigating your retirement plan can sometimes feel like piloting a ship through a stormy sea. Employee Retirement Income Security Act (ERISA), enacted in 1974, serves as the guiding lighthouse to help steer your ship to safe harbor U.S. Department of Labor.

One of the most significant ways ERISA impacts retirement plans is by ensuring fair play. It mandates that plan fiduciaries, those managing your retirement plan, must act solely in your interest, guarding against potential mismanagement or misuse of funds Investopedia. Knowing that your hard-earned money is under watchful eyes can provide invaluable peace of mind.

Furthermore, ERISA requires your plan administrators to regularly provide you with detailed, easy-to-understand information about your plan. This transparency helps you understand where your money is going, empowering you to make informed decisions about your future.

B. How ERISA Protects Your Retirement Benefits

ERISA’s influence extends beyond just regulating retirement plans — it also actively protects your retirement benefits.

One such protective measure is the guarantee of certain benefits through the Pension Benefit Guaranty Corporation (PBGC), even if your plan is terminated. This financial safety net provides assurance that, no matter what, you will receive the benefits you’ve earned.

ERISA also ensures vesting rights, meaning you acquire a non-forfeitable right to your retirement benefits after meeting certain requirements Investopedia. This means that even if you change jobs, your accrued benefits remain yours — they’re locked away safe and secure.

Additionally, ERISA provides for survivor benefits, ensuring your spouse is protected in the event of your death U.S. Department of Labor. Isn’t it reassuring to know ERISA is looking out for both you and your loved ones?

ERISA’s role in retirement planning is undeniably significant. From setting minimum standards for private-sector plans to protecting your retirement benefits, ERISA offers a level of security that every retiree or future retiree should understand.

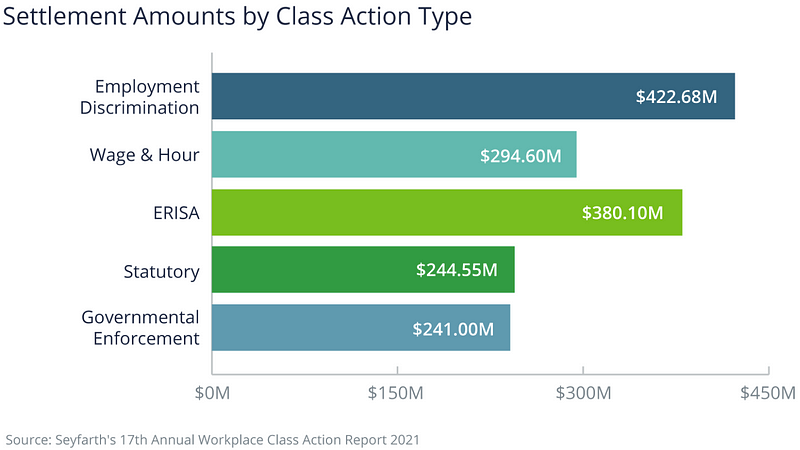

Figure Legend: Seyfarth’s 2021 report showed ERISA class action settlements totaled $380.01M, a slight rise from previous years.

2. ERISA Covered Retirement Plans: Your Beneficiary’s Safety Net

A. The Role of ERISA in Beneficiary Protection

Like a knight in shining armor, ERISA doesn’t only protect you — it extends its protective cloak to your beneficiaries as well. But how exactly does ERISA contribute to beneficiary protection?

The answer lies in ERISA’s firm stance on default beneficiary designations Cornell Law School. If you’re married, your spouse is automatically considered the beneficiary of your ERISA-covered retirement plan, unless they waive this right. It means that even if you forget to designate a beneficiary or the designation isn’t legally valid, your spouse will still be entitled to your benefits. ERISA ensures that your better half won’t be left out in the cold.

For non-spouse beneficiaries, ERISA still plays a significant role. Although they don’t receive the same level of protection as a spouse, ERISA allows for the transfer of your retirement benefits to them. This guarantees that your hard-earned savings can provide for your loved ones long after you’re gone.

B. Benefits of Designating an ERISA Retirement Plan Beneficiary

Designating a beneficiary for your ERISA-covered retirement plan is not just a good idea — it’s a crucial step in managing your retirement assets. This designation determines who inherits your retirement benefits. But why is this so important?

By designating a beneficiary, you decide who receives the benefits in the event of your death. It could be your spouse, children, or even a charitable organization.

Designating an ERISA retirement plan beneficiary also provides certain tax advantages. With proper planning, your beneficiary can minimize taxes on inherited retirement assets, allowing them to reap the full benefits of your savings.

3. Navigating the ERISA Beneficiary Rules: A Step-by-Step Guide

A. Key Rules to Consider When Designating an ERISA Beneficiary

Here are some key rules to keep in mind U.S. Department of Labor.

Firstly, if you’re married, your spouse is automatically your ERISA retirement plan beneficiary. If you want to name someone else, your spouse must provide written consent. Think of this rule as the compass guiding your journey IRS.

Secondly, you may name multiple beneficiaries and specify the percentage of benefits each should receive.

Thirdly, you can change your beneficiary at any time, provided it’s done according to plan rules. It offers flexibility as your life circumstances change.

B. Common Mistakes to Avoid in Beneficiary Designation

One common error is forgetting to update your beneficiaries following major life events like marriage, the birth of your kid, or divorce.

Another mistake is failing to consider the tax implications for your beneficiaries. Inheritance tax can take a large bite out of your hard-earned treasure if not properly planned.

Lastly, not properly communicating your plans with your beneficiaries can lead to confusion and disputes. It’s like leaving your family without a clear direction.

4. Enhancing Your Financial Legacy: The ERISA Advantage

A. The Role of ERISA in Wealth Transfer

Imagine your accumulated retirement benefits as a vast treasury, and you’re the monarch who wishes to pass this wealth onto the next generation. Here’s where ERISA enters the scene, playing the pivotal role of the royal advisor, helping ensure a smooth and legally-sound transition of your assets.

Employee Retirement Income Security Act (ERISA) safeguards your spouse’s rights to your retirement benefits after your passing. Further, ERISA provides flexibility in designating non-spousal beneficiaries, be it your children, friends, or charitable organizations, turning your retirement funds into a lasting legacy IRS.

B. Impact of ERISA on Inheritance Tax and Your Heirs

To paint a clearer picture, let’s say your heir inherits your ERISA-covered retirement account. Depending on the size of the inheritance, they might face a significant tax burden. However, the silver lining here is that, under certain conditions, your heirs could stretch out the distributions over their lifetime, potentially reducing the annual tax hit IRS.

Understanding how ERISA impacts inheritance tax and your heirs is akin to understanding the trade winds. It can help ensure a smooth sail for your heirs as they navigate their own financial seas. ERISA can offer you the advantage you need to transfer your wealth effectively and efficiently.

5. Case Study: Real-World Examples of ERISA Beneficiary Designations

A. Success Stories: Effective Use of ERISA in Retirement Planning

To understand the power of ERISA in action, let’s look at a hypothetical but representative case — let’s call him John. John had a considerable retirement fund and a clear beneficiary — his wife. When he passed away, his wife received the retirement funds without any legal complications or unexpected tax liabilities, thanks to the spouse-protecting clause in ERISA. John’s story exemplifies the effective use of ERISA in safeguarding spousal retirement benefits.

Next, consider Jane, a charitable person who never married or had children. She designated a non-profit organization as her ERISA retirement plan beneficiary. After her passing, her retirement savings went directly to the cause she supported IRS. Her story showcases how ERISA can help turn retirement funds into a lasting legacy.

B. Lessons Learned: Pitfalls and How to Avoid Them

Now, on the flip side, there are cautionary tales. Meet Robert, who overlooked updating his beneficiary designations post-divorce. Upon his passing, the retirement funds unintentionally went to his ex-spouse, much to his children’s dismay. This situation highlights the importance of timely updates to beneficiary designations to avoid unintended consequences.

Similarly, consider Emily’s case, who named her minor grandchild as the beneficiary. Unfortunately, due to legal restrictions regarding minors, the process to access the funds became complex and time-consuming. Emily’s case illustrates the need for careful consideration when designating minors as beneficiaries.

These real-world examples underscore the crucial role of ERISA in retirement planning, providing lessons in both its effective use and common pitfalls to avoid.

6. Your Action Plan: Strategies for Effective ERISA Retirement Planning

A. Expert Tips for Optimizing ERISA Retirement Plans

When it comes to utilizing ERISA for your retirement planning, there are several strategies to consider.

Firstly, remember the mantra “Review, Revisit, and Revise”. ERISA retirement plans should not be a ‘set-and-forget’ situation. Life events like marriage, birth, divorce, or death can dramatically impact your plan. Regularly reviewing and updating your beneficiary designations to match your current life circumstances is paramount.

Secondly, if you have multiple beneficiaries, consider the Separate Account Rule. By dividing your retirement account into separate shares for each beneficiary, you allow each heir to use their own life expectancy for Required Minimum Distributions (RMDs), potentially allowing for more tax-efficient wealth transfer.

Thirdly, if you’re charitably inclined, ERISA enables you to make a significant impact even after your lifetime. You can designate a charitable organization as your beneficiary, ensuring your legacy continues to support causes you care about.

B. How to Seek Professional Help for ERISA Planning

While it’s possible to navigate ERISA on your own, the laws and regulations can be complex. Seeking professional advice can provide valuable guidance and peace of mind.

Financial advisors, with their vast experience and deep understanding of ERISA, can help you make the most out of your retirement plan. They can guide you in optimizing your plan for tax-efficiency, maintaining compliance with ever-changing laws, and ensuring your wealth transfer goals are achieved.

Additionally, attorneys specializing in estate planning can help you understand the implications of your decisions and provide legal strategies for wealth preservation and transfer.

7. A Deep Dive into ERISA Beneficiary Designations and Fiduciary Duties

A. Understanding the ERISA Beneficiary Designation Form: A Key Tool for Plan Participants

So, what is ERISA Beneficiary Designation Form? Essentially, it is a legally binding document that specifies who will receive your retirement plan assets upon your death. The importance of this form for plan participants cannot be overstated.

By completing this form, you get to nominate your primary beneficiaries — these are the individuals who are first in line to receive your retirement benefits. Typically, these are your spouse or children. However, it doesn’t stop there. Life is unpredictable, and the form offers an extra layer of preparedness through what’s called contingent beneficiaries.

Contingent beneficiaries are essentially your backup plan. In the unfortunate event that a primary beneficiary predeceases you or chooses to disclaim the benefits, the contingent beneficiaries will then be eligible to receive your retirement assets.

Don’t underestimate the power of this form. Keep it updated, keep it accurate, and above all, make it an integral part of your retirement planning strategy.

B. The Role of the Plan Sponsor in ERISA Employee Benefit Plan

A plan sponsor is a designated party — usually an employer or a company — who sets up an ERISA employee benefit plan for the benefit of the organization’s employees. This isn’t just a ceremonial title, it carries real responsibilities.

One of the significant responsibilities of the plan sponsor is to ensure the plan’s adherence to ERISA standards, including fiduciary requirements. Fiduciary duty, in this case, means that the plan sponsor is required to support the interest of the plan participants. This involves making prudent decisions about the plan’s investments, minimizing fees, and following the plan terms.

However, the role of the plan sponsor extends beyond just managing the plan. Clear and consistent communication between the plan sponsor and the plan participant is crucial. Have you ever played the game of ‘telephone’, where a message gets distorted as it is passed along? In the world of ERISA retirement planning, we can’t afford such distortions.

That’s why plan sponsors are also tasked with keeping the plan participants informed about the plan’s features, benefits, and rights. This includes providing regular updates on the plan’s performance, ensuring the plan participant has a clear understanding of the terms, conditions, and status of their retirement plan.

To sum up, think of your plan sponsor as your retirement planning relay partner, carrying the baton of responsibility, and making sure that your race towards financial security is a winning one!

C. Balancing Fiduciary Duties in ERISA Covered Retirement Plans

Imagine being on a tightrope, trying to keep your balance while walking towards a prize — financial security in retirement. This is similar to how fiduciaries must balance their responsibilities in managing ERISA covered retirement plans. So, let’s break down what it truly means to carry the weight of these fiduciary duties.

A fiduciary in the ERISA context is any person who exercises discretionary authority or control over a retirement plan’s management or assets, or gives investment advice for a fee. This role is not for the faint of heart — it’s a position of trust and a pledge to put the participants’ best interest first, always.

But what does this fiduciary requirement entail in real-world scenarios? Imagine you’re a passenger on a plane. You’d want the pilot to be highly competent, right? Fiduciaries, like those pilots, must act with the care, skill, prudence, and diligence under the circumstances that a prudent person acting in a similar capacity would use in a similar situation. No reckless financial maneuvering is allowed here.

So how do fiduciaries ensure the rights and benefits of plan participants? Much like a pilot communicates with air traffic control, fiduciaries need to maintain an open channel of communication with plan participants. Fiduciaries must provide participants with important information about the plan, including its features, funding, and management.

Finally, fiduciaries must ensure that the benefits due to the plan participants are available when they retire or when the time comes to pass these benefits to their beneficiaries. This role’s weight may seem daunting, but it is crucial for ensuring the integrity of the retirement system.

D. What Happens at the Time of Death: Navigating Death Benefits

Imagine a relay race where a baton is passed from one runner to another. Here, the baton represents your retirement savings, and the runners are your beneficiaries. The person who first gets the baton is your primary beneficiary. Often, this is your spouse or child, but it could be anyone you choose.

But what if, in our relay race, the primary runner is unable to accept the baton? Enter the contingent beneficiary. They’re like the reserve runner, ready to take the baton if the primary runner can’t. The contingent beneficiary can be an individual, trust, charity, or even your estate. They ensure that your baton, your legacy, stays in the race even when unforeseen hurdles arise.

The beneficiary must file a claim with the plan administrator, who then has a duty to provide a decision within a reasonable time, generally 90 days. If the claim is denied, the plan must provide a written notice explaining the reasons and offering the beneficiary a chance to appeal. It’s a structured, step-by-step race, keeping the transfer of your hard-earned savings transparent and fair.

So, how do we ensure a seamless baton pass, a smooth transfer of benefits? First, regularly review and update your beneficiary designations, especially after significant life events like marriage, divorce, or your newborn child. This is like ensuring that your chosen runner is ready and able to take the baton.

Second, consider sharing relevant information about your retirement plan with your beneficiaries — plan name, policy number, and the plan sponsor’s contact information. This is akin to giving your runners the race details — the when, where, and how of the baton pass.

Finally, consult with a financial advisor or attorney to understand the tax implications for your beneficiaries. Just as runners prepare for the weather conditions on race day, understanding these implications can help your beneficiaries be prepared when they receive the baton.

Conclusion

Smart planning with ERISA doesn’t just secure your retirement — it creates a financial legacy for your loved ones. Understanding the beneficiary designation form, maintaining clear communication with your plan sponsor, balancing fiduciary duties, and ensuring a seamless transition of benefits at the time of death are all critical components of this journey.

Remember, you are not just planning for retirement, but for a legacy that spans generations. Your strategic planning today can create a lifetime of security for those you care about most.

It’s never too early or too late to start. Seek expert guidance, learn from real-world case studies, and lean on professional assistance to navigate the complexities of ERISA.

Frequently Asked Questions (FAQ)

What is the importance of the ERISA Beneficiary Designation Form?

The ERISA Beneficiary Designation Form is crucial as it dictates who will receive your ERISA-governed retirement benefits after your death. Completing this form ensures that your benefits will be distributed according to your wishes.

What roles do the Plan Sponsor and Fiduciaries play in ERISA-covered retirement plans?

The Plan Sponsor establishes the plan and selects the service providers. They also have the responsibility to monitor the plan’s operation. Fiduciaries are those who exercise discretionary authority or control over the plan’s management or assets. They must act in the interest of the plan participants and beneficiaries, providing benefits and cover expenses to implement the plan.

What are the basic differences between a Contingent and Primary Beneficiary in ERISA?

A Primary Beneficiary is the first person (or persons) who will receive your benefits upon your death. If the primary beneficiary predeceases you, or chooses to disclaim the benefits, the Contingent Beneficiary will then receive the benefits.

What happens to my ERISA benefits when I die?

Your benefits will be distributed to your designated beneficiaries upon your death. It’s essential to keep your beneficiary designations up-to-date to ensure the benefits are distributed according to your wishes.

Can I seek professional help for ERISA planning?

Yes, navigating ERISA can be complex, and seeking help from a financial advisor or an ERISA expert can be highly beneficial. They can provide advice and help you optimize your retirement plans to secure your financial legacy.