Summary:

Securing a comfortable retirement requires strategic planning, and our blog post delves into the key aspects that you should consider. It all begins with assessing your retirement goals and aligning your pension plan accordingly. Understanding tax implications, diversification, and risk management strategies can help you maximize your retirement savings. Be it optimizing Social Security benefits, navigating employer-sponsored retirement plans and minimum distributions, or diversifying your investment portfolio — every facet of your retirement income should be considered carefully. Additionally, knowing the role of insurance companies in retirement can aid in making informed decisions. Importantly, seeking professional help from a financial advisor can provide you with tailor-made strategies. To conclude, maximizing your tax-deferred pension and savings plans is a critical step towards achieving a stress-free retirement. Remember the wise words of Benjamin Franklin — “An investment in knowledge pays the best interest”. Take action today, and secure a prosperous tomorrow.

Introduction

Imagine a future where you can truly embrace the freedom of retirement without the worry of financial insecurity hanging over your head. A future where your hard-earned savings continue to grow, safeguarding you against the unforeseen and allowing you to enjoy the rewards of years of diligent work. This isn’t a pipe dream, but a reality you can create with the strategic use of tax-deferred pension and retirement savings plans.

Navigating the financial aspects of retirement can feel like trying to find your way through a labyrinth, with tax codes, financial jargon, and a myriad of investment options. But, what if there was a key that could simplify this complexity and unlock the door to financial security?

This blog post aims to demystify tax-deferred pensions and retirement savings, to help you understand their power and potential, and to guide you in making decisions that will secure your future.

1. The Power of Tax-Deferred Growth

A. How Tax-Deferred Growth Works

In the grand game of retirement planning, tax-deferred growth is like having a secret weapon. But what exactly does “tax-deferred” mean, and how does it work? Picture your retirement fund as a small tree. Just as a tree needs time, sunshine, and water to grow, your retirement fund requires time, initial investment, and the magic of compound interest.

A tax-deferred retirement plan is like a greenhouse for this financial tree. Your contributions, or the seeds, are often made with pre-tax dollars, meaning you don’t pay income taxes on the money you invest initially. Now, within this tax-free greenhouse, your investments start to grow. And as they grow, the earnings — the fruits of your investment tree — aren’t taxed until you start to withdraw them during retirement.

This system allows your investments to compound over time without the drag of yearly taxes. Like a snowball rolling down a hill, it accumulates more and more mass (or in this case, wealth) as it keeps rolling, resulting in a larger fund for you in the future.

B. Long-term Advantages of Tax-Deferred Growth

First, tax deferral means more of your money is working for you right away. If you’re in the 22% tax bracket, every $1,000 you contribute effectively becomes $780 in a taxable account but remains $1,000 in a tax-deferred account. That’s more money planted in your greenhouse right from the start.

Over time, the power of compounding amplifies this difference. Let’s say you invest $5,000 per year for 30 years. In a taxable account with a 15% tax drag and 7% growth, you’d end up with roughly $389,000. But in a tax-deferred account with the same growth, you’d accumulate over $505,000. That’s a difference of more than $116,000. In the long run, that could mean extra years of comfortable retirement or a significant legacy for your heirs. This illustrates the power of tax-deferred growth.

Moreover, tax-deferred accounts give you more control over your tax situation. When you begin to withdraw your funds in retirement, you might be in a lower tax bracket, effectively reducing the amount you have to pay.

2. The Role of Pension and Retirement Savings Plans in Financial Security

A. Understanding Your Pension Plan Options

Navigating the labyrinth of pension plans can feel like being dropped into a foreign city without a map.

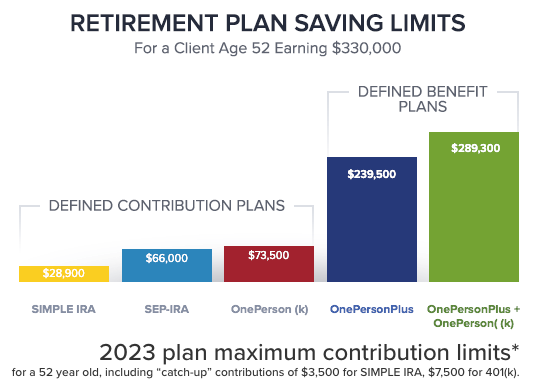

There are two major types of pension plans: defined benefit plans and defined contribution plans. A defined benefit plan, often seen as the golden child of pension plans, promises a specific monthly benefit at retirement, calculated through a formula involving your salary, age, and years of service. Sounds simple, right? However, these defined benefit plans are becoming rarer in the private sector.

In contrast, defined contribution plans, like 401(k)s or 403(b)s, are more like a DIY project. You and possibly your employer contribute money to your individual account, and the future benefits are based on how much was contributed and how well the investment performs. These types of plans put more responsibility on your shoulders, but also give you more control over your retirement savings.

Figure Legend: Comparing contribution limits for contribution plans vs benefit plans.

B. Building a Solid Retirement Savings Strategy

First, take full advantage of your employer’s retirement savings plan, especially if they match your contributions. This is essentially free money, an added bonus to your savings that can compound over time. However, don’t put all your eggs in one basket. Diversifying your retirement savings through IRAs, for example, can offer additional tax advantages and increase your overall savings.

And don’t forget about the power of tax-deferred growth we discussed earlier. Making use of tax-deferred accounts can supercharge your savings, giving your money the chance to grow unhindered by yearly taxes.

But no castle can stand without a solid foundation. For your retirement savings strategy, this foundation is a clear understanding of your financial goals, risk tolerance, and retirement timeline. Tools like retirement calculators can provide a valuable starting point.

3. Navigating the Complexities of Tax-Deferred Pension Plans

A. Common Misconceptions and Pitfalls

Like venturing into a dense forest, entering the world of tax-deferred pension plans can be full of complexities and challenges. To navigate this terrain, you must first be aware of the common misconceptions and pitfalls.

Misconception 1: “I don’t need to start saving now; I have plenty of time.” This procrastination trap can severely hinder your potential for growth. Remember, with tax-deferred pension plans, time is your best friend, as compound interest is the magic formula that makes your money multiply.

Misconception 2: “I don’t make enough money to save for retirement.” No matter how small the contribution, every dollar saved today can grow into a sizable nest egg thanks to compound interest and tax-deferred growth.

Misconception 3: “I can withdraw money from my pension plan without penalties.” Beware! Early withdrawals before the age of 59 1/2 from most tax-deferred pension plans can lead to hefty penalties and income tax charges.

Pitfall 1: Ignoring diversification. Focusing on a single type of investment can expose your savings to unnecessary risks. Diversification can provide a safety net.

Pitfall 2: Not reevaluating your retirement strategy. It’s essential to regularly assess and adjust your retirement savings strategy based on life changes and market trends.

B. The Right Way to Approach Tax-Deferred Pension Plans

Navigating tax-deferred pension plans can be smooth sailing if you know how to steer the ship.

Step 1: Start Early and Consistently Save: Make the power of compound interest work in your favor. The earlier you start, the more time your money has to grow.

Step 2: Diversify Your Portfolio: Spread your investments across a variety of assets to mitigate risk and optimize potential returns.

Step 3: Avoid Early Withdrawals: Resist the temptation to dip into your retirement savings. The penalties and lost growth potential can be detrimental to your long-term financial health.

Step 4: Keep Learning: Stay informed about the changes in tax laws and retirement savings strategies.

Step 5: Seek Professional Advice: Consider consulting a financial advisor who specializes in retirement planning. They can offer personalized advice tailored to your unique circumstances and help steer you clear of common pitfalls.

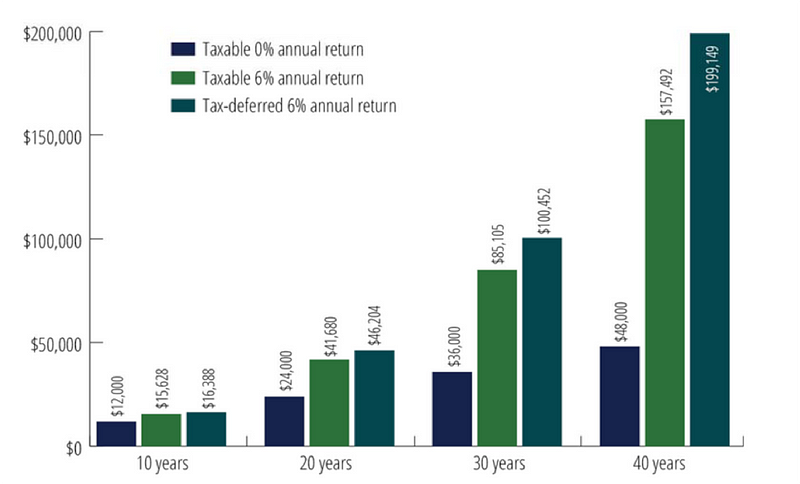

Figure Legend: This illustration compares tax-deferred and taxable investments, assuming $100 monthly contributions and a 15% tax bracket. It’s not financial advice or a future prediction. Rates may vary, and tax implications exist. The example doesn’t account for fees, which could reduce the tax-deferred accumulation shown.

4. Case Study: Real-life Success Stories of Tax-Deferred Pensions and Retirement Savings

A. Insight from Successful Retirees

Let’s delve into the insights from a couple of successful retirees who maximized their tax-deferred pensions and retirement savings.

Case 1: Reflect upon the story of Anne Scheiber, a low-paid IRS auditor who left a $22 million fortune. She led a frugal lifestyle, and invested her savings in blue-chip stocks, reinvesting all the dividends.

Case 2: Consider the story of Sylvia Bloom, a legal secretary who amassed an impressive $9 million fortune. Her secret? Consistently investing a portion of her income and maintaining a diversified portfolio of investments, as detailed in this New York Times article.

B. Lessons Learned and Best Practices

The successful retirees’ stories inspire us, and their experiences impart valuable lessons.

Lesson 1: Start Early: As Scheiber’s story proves, the sooner you start saving and investing, the more time your investments have to grow.

Lesson 2: Invest Consistently: Both Scheiber and Bloom demonstrated that regular investments are key to building a substantial retirement fund.

Lesson 3: Diversify: Bloom’s story highlights the importance of a diversified investment portfolio. Diversification can reduce risk and enhance growth opportunities.

Lesson 4: Be patient: Scheiber’s investing strategy shows us the importance of being patient and holding onto good stocks for the long term.

5. Securing Your Future with Tax-Deferred Pension and Retirement Savings Plans

A. Assessing Your Retirement Goals

Defining your retirement goals is the first step towards securing your future. The question is, how do you envision your golden years? Do you see yourself traveling the world, enjoying leisurely pursuits, or perhaps pursuing a hobby? Or maybe your goal is to simply maintain your current lifestyle post-retirement? By understanding what you want from retirement, you can plan effectively.

This Forbes article can provide a more comprehensive understanding of how to assess your retirement goals.

B. Aligning Your Pension Plan with Your Retirement Vision

After defining your goals, it’s crucial to ensure your pension plan aligns with them. Consider the lifestyle you wish to lead post-retirement. Will your current plan support that lifestyle? Or do you need to make adjustments? Keep in mind, the path to financial security in retirement isn’t one-size-fits-all. It requires customizing your savings and investment strategies to your individual goals and circumstances.

Take advantage of tax-deferred pension and retirement savings plans to maximize your savings. Understand the different types of retirement accounts available to you. From 401(k)s and 403(b)s to traditional IRAs and Roth IRAs, each offers unique tax advantages that can significantly boost your retirement savings.

But don’t stop there. Regularly review and adjust your plan as needed. Life happens. Your goals may change, and market conditions fluctuate. Make sure your retirement savings strategy adapts accordingly. Consult with a trusted financial advisor or planner to help navigate these complexities.

An article from the Financial Industry Regulatory Authority (FINRA) can offer additional insight into aligning your pension plan with your retirement vision. And remember, it’s never too early or too late to start planning. Every step you take now brings you closer to a more secure future.

6. Key Considerations for Your Retirement Savings Strategy

A. Tax Implications and Strategies

One of the key elements to consider when strategizing for retirement savings is understanding tax implications. The type of retirement savings account you choose can have a significant impact on your future tax liabilities.

For instance, traditional IRA contributions are tax-deductible, and your earnings grow tax-deferred until you withdraw the funds. On the other hand, Roth IRA contributions are made with after-tax dollars, meaning that the earnings and withdrawals are tax-free. This IRS guide can provide a deeper insight into traditional and Roth IRAs.

Understanding tax implications can help you optimize your retirement savings strategy. The tax deferral benefit provided by retirement accounts allows your investments to compound over time without being reduced by taxes.

B. Diversification and Risk Management

In addition to understanding tax implications, diversification is crucial for a robust retirement savings strategy. It involves spreading your investments across a variety of asset classes such as stocks, bonds, and cash equivalents to mitigate risk.

Remember the old adage, “Don’t put all your eggs in one basket”? That’s precisely what diversification is about. It safeguards you from bad investments. Diversification, however, doesn’t guarantee profits or protect against loss in declining markets.

Risk management goes hand in hand with diversification. As you near retirement, you might want to adopt a more conservative approach to investing to protect your accumulated savings. This Vanguard article provides a detailed understanding of investment risks and how to manage them.

7. Leverage Tax-Deferred Pension for a Stress-Free Retirement

A. Tips for Maximizing Your Pension Plan

To truly leverage your tax-deferred pension for a stress-free retirement, here are some key strategies to consider:

- Start Early and Maximize Contributions: The power of compounding is truly magical, and it works best when given time. Hence, start contributing to your pension plan as early as possible. Also, try to contribute the maximum allowable amount each year to enjoy greater tax-deferred growth.

- Take Full Advantage of Employer Matches: If your employer offers a matching contribution, be sure to contribute at least up to that match. It’s essentially free money being added to your retirement nest egg.

- Consider Catch-Up Contributions: If you’re over 50, take advantage of catch-up contributions which allow you to contribute more than the annual limit to your retirement accounts.

- Avoid Early Withdrawals: Early withdrawals not only incur penalties but also hamper the compounding effect of your savings. You can refer to this article from IRS to learn more about the penalties on early withdrawals.

B. Getting Professional Help: The Role of a Financial Advisor

Financial advisors can provide personalized advice based on your financial goals, risk tolerance, and time horizon. They can help you understand the nuances of different pension plans, optimize your contributions, and design a diversified investment strategy that aligns with your retirement vision.

However, remember that not all advisors are good for retirement planning. Choose someone who acts as a fiduciary — an advisor who can act in your best interests. This guide by Consumer Financial Protection Bureau offers detailed advice on choosing the right financial advisor.

8. Maximizing Your Retirement Income: Social Security, Employer-Sponsored Plans, and Investment Strategies

A. Understanding Social Security and Your Retirement Benefits

Social Security serves as a lifeline for many retirees, acting as a steady stream of income that keeps the boat afloat when regular employment checks stop coming in. However, it’s more than just a lifesaver — by fully understanding how to maximize your Social Security benefits, you can turn this lifeline into a sturdy sail, propelling your retirement journey forward.

Did you know that the age you decide to retire impacts the size of your Social Security checks? It’s a bit like baking a cake — the longer you let it bake (or the longer you wait to retire), the bigger and better it gets. Learn more about when to claim your social security benefits and maximize your income.

B. Navigating Employer-Sponsored Retirement Plans and Minimum Distributions

Consider your employer-sponsored retirement plan as the compass guiding you through the unchartered territory of retirement. These plans, whether they be 401(k)s or IRAs, offer different paths with varying degrees of risk and reward.

Like the tides that ebb and flow, minimum distributions are the law of the sea when it comes to retirement plans. Understanding them is critical, as they play a pivotal role in retirement planning. There are strategies available that can help you navigate these waters and maximize the benefits of your plan.

C. Incorporating Investments into Your Retirement Income

The key to a sturdy retirement ship is a diversified investment portfolio. It’s a bit like assembling a crew — you wouldn’t sail with only navigators, would you? Instead, you need a mix of roles. In the same way, a well-rounded portfolio includes a variety of investments, such as stocks, bonds, and mutual funds. Learn how to diversify your portfolio to spread the risk and optimize returns.

But beware, pirates lurk in these waters — and in retirement planning, they come in the form of taxes. Understanding the tax implications of your investment income during retirement is crucial.

D. The Role of Insurance Companies in Retirement Planning

Lastly, let’s not forget about the role insurance companies play in this voyage. They offer a myriad of products, like annuities and life insurance, which can be vital lifeboats in your retirement strategy. However, it’s essential to consider factors like fees and the financial strength of the company before hopping on board. Here’s what to consider before buying annuities.

Conclusion

Planning for retirement can seem like a daunting task, but it doesn’t have to be. With the right knowledge and approach, you can build a robust retirement savings strategy that leverages the power of tax-deferred pension plans. This will not only help you build a sizable nest egg but also offer the peace of mind that comes with financial security.

With tax-deferred pension plans, you can actualize this wisdom in a way that maximizes your savings while minimizing your tax liabilities.

So, what’s your next move? Start today. Review your retirement goals, understand the pension plans at your disposal, and be strategic about your savings. Consider getting professional help if needed. Remember, every day counts when it comes to saving for retirement.

To empower yourself further, engage with our other articles on pension plans and retirement savings. Equip yourself with the knowledge you need to navigate your financial future confidently. You’ve worked hard for your money; now it’s time to make your money work hard for you.

Don’t just dream about a stress-free retirement — start planning for it today.

Frequently Asked Questions (FAQ)

How can I maximize my Social Security benefits and retirement savings from employer-sponsored plans?

You can maximize your benefits by understanding how Social Security and retirement benefits work. Planning your retirement age, understanding the role of minimum distributions, and exploring strategies to get the most out of your employer-sponsored retirement plan can be beneficial.

How can investment and insurance companies play a role in my retirement planning?

Investments can provide additional income during retirement. Diversifying your investment portfolio and understanding the tax implications is essential. Insurance companies offer retirement products that can complement your retirement income strategy.

Can I manage my retirement planning on my own, or do I need professional help?

While it is possible to manage your retirement planning independently, seeking professional help can provide valuable insights tailored to your financial situation and goals. Financial advisors can help you navigate the complexities of retirement planning.

How can I learn from successful retirees?

Studying real-life success stories can provide you with practical strategies for retirement savings. For instance, Grace Groner and Ronald Read, who turned modest savings into substantial retirement funds, exemplify the power of consistent saving and smart investment strategies.

What are the key considerations when developing a retirement savings strategy?

The main considerations include understanding your retirement goals and aligning your pension plan accordingly. This involves knowing the tax implications, developing a risk management strategy, and diversifying your investments.